TL;DR:

- Exchange rates significantly impact the actual amount recipients receive when sending money abroad by including provider markups and FX margins. Small rate differences can amount to hundreds of dollars annually, highlighting the importance of comparing total net amounts rather than just fees or advertised rates. Using real-time comparison tools and monitoring market trends enables smarter transfers and minimizes hidden costs.

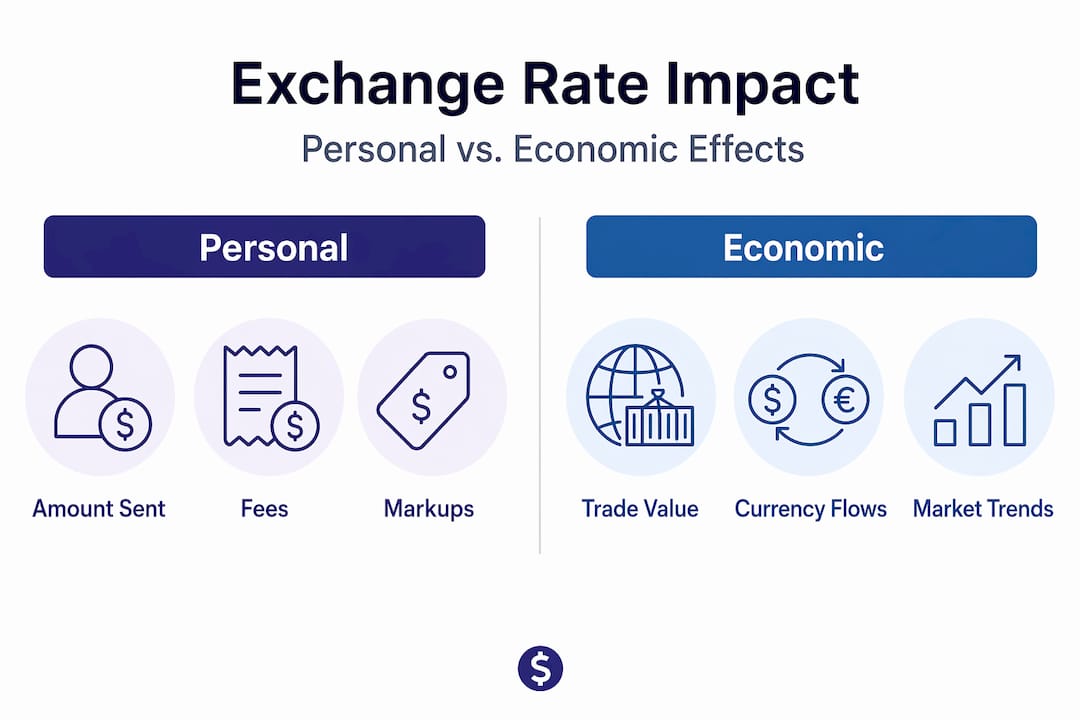

Every time you send money abroad, an exchange rate determines how much your recipient actually gets. That number is rarely the one you see advertised. The role of exchange rates in remittance is more complex than most people realize, and the gap between a great rate and a poor one can cost you hundreds of dollars per year. Whether you send money to family in Morocco, the Philippines, or Mexico, understanding how exchange rates work will help you make smarter decisions and stop leaving money on the table.

Table of Contents

- Key takeaways

- The role of exchange rates, explained simply

- How exchange rates affect your remittances

- Exchange rates and their broader economic role

- Managing exchange rate risk as a sender

- My take on the real cost hiding in plain sight

- Find the best rate for your next transfer

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Rates differ by provider | Every provider adds a markup to the mid-market rate, directly reducing how much your recipient receives. |

| Small differences add up fast | A 20-naira gap per dollar means 10,000 fewer naira on a $500 transfer. |

| Fees and rates both matter | Always calculate the net amount received, not just the advertised fee or rate alone. |

| Timing affects outcomes | Exchange rate volatility means the same transfer sent on different days can yield very different amounts. |

| Comparison tools save money | Using a platform that shows real-time rates and total costs helps you find the best deal quickly. |

The role of exchange rates, explained simply

An exchange rate tells you how much one currency is worth in another. When you send U.S. dollars to a recipient in Nigeria, the exchange rate converts those dollars into naira. The higher the rate, the more naira your recipient gets for every dollar you send.

There are two types you should know about. The nominal exchange rate is the face-value price between two currencies. The real exchange rate adjusts for price differences between countries and reflects actual purchasing power. For everyday money transfers, the nominal rate is what matters most.

Every currency pair, such as USD/MXN or GBP/PHP, has a mid-market rate. This is the midpoint between the buy and sell prices on global currency markets, and it's the rate you'll see on Google or financial news sites. Banks and transfer providers almost never offer this rate to customers. Instead, they add a markup, sometimes called a spread, and that markup becomes their profit.

- The mid-market rate is the fairest exchange rate available, but it is not publicly accessible for personal transfers.

- Buy rates and sell rates reflect what providers pay and charge, respectively.

- Markups typically range from 0.5% to 5%, depending on the provider and currency corridor.

- Financial market activities like carry trades and leverage can amplify exchange rate movements significantly.

Pro Tip: Search for the current mid-market rate on Google before initiating any transfer. It gives you a benchmark to measure how much markup a provider is charging.

How exchange rates affect your remittances

This is where the role of exchange rates in money transfers becomes very personal. Providers set their own exchange rate prices, which directly affects how much your recipient gets at the end of the transfer. A provider that advertises zero fees but offers a rate that is 3% below the mid-market rate is still charging you. The cost is just hidden inside the conversion.

Consider this real-world illustration: a 20-naira difference per dollar results in 10,000 fewer naira on a $500 transfer. That is a meaningful sum for a family relying on remittances to cover rent or school fees. Multiply that across 12 monthly transfers, and you are losing the equivalent of two full transfers per year.

Here is a simplified comparison of how different providers might handle a $500 transfer to Nigeria:

| Provider | Exchange rate (USD/NGN) | Transfer fee | Amount received (NGN) |

|---|---|---|---|

| Traditional bank | 1,520 | $10.00 | 750,800 |

| Provider A | 1,545 | $4.99 | 769,765 |

| Provider B | 1,560 | $2.99 | 778,350 |

| Provider C | 1,570 | $0.00 | 785,000 |

The differences look small in rate terms, but cross-border remittance fees total about 6.35% on average for low-income countries when factoring in both fees and FX margins. That percentage represents real money leaving your family's pocket.

Why do providers offer such different rates? It comes down to their business model, operational costs, and how they manage their own currency risk. Fintech providers often operate with lower overhead, allowing them to offer tighter margins. Traditional banks, by contrast, carry heavier infrastructure costs and typically pass those along in the form of wider spreads.

- Always ask for or calculate the total amount your recipient will receive before confirming a transfer.

- Compare providers on the net amount delivered, not on advertised fees alone.

- Currency corridors matter. Some routes are more competitive than others depending on volume and regulation.

- The actual amount received is the only number that truly counts when evaluating a transfer service.

Pro Tip: Use a comparison tool that shows you total recipient amount across multiple providers side by side. A few minutes of research can save you more than the transfer fee itself.

Exchange rates and their broader economic role

The role of currency conversion extends far beyond personal transfers. Exchange rates act as a common basis for valuing goods and services across borders, and they directly shape how competitive a country's exports and imports are on the world stage.

When a country's currency depreciates, its exports become cheaper for foreign buyers, which can stimulate demand and boost GDP. At the same time, imports become more expensive, which can contribute to domestic inflation. This two-sided effect means exchange rate movements ripple through everything from grocery prices to manufacturing jobs.

Here is how exchange rate shifts affect trade and the broader economy:

- Export competitiveness: A weaker currency makes locally produced goods cheaper for international buyers, often increasing export volumes.

- Import costs: A stronger currency makes foreign goods more affordable domestically, which can lower prices but hurt local manufacturers.

- Inflation pressure: When import prices rise due to currency depreciation, those costs often pass through to consumers, a phenomenon called imported inflation.

- Remittance inflows: Large-scale remittances can appreciate a country's real effective exchange rate, particularly in high-remittance economies. This can reduce export competitiveness over time, a dynamic consistent with Dutch disease effects.

- Financial market stability: Strong domestic financial markets help buffer exchange rate volatility caused by remittance surges, reducing the disruptive economic impact.

For anyone sending money internationally, understanding these dynamics provides useful context. The exchange rate you transact at today is shaped by forces far larger than any single transfer service.

Managing exchange rate risk as a sender

The effects of currency fluctuations can work for you or against you depending on when you send. A rate that looks good on Monday might be 2% worse by Thursday. For people sending large amounts or transferring regularly, this volatility deserves real attention.

Some providers lock in rates to protect senders against market swings during the transfer window. Others pass fluctuations directly to the customer, meaning the rate you see when you initiate a transfer might differ slightly from the rate applied when the transfer executes. Knowing which model your provider uses matters.

Here are practical steps to manage exchange rate risk effectively:

- Know your benchmark. Check the mid-market rate before every transfer so you know how large the markup is.

- Monitor rate trends. If your destination currency has been weakening, waiting a few days might improve what your recipient receives.

- Set rate alerts. Several transfer platforms, including Idealremit, allow you to receive a notification when your target rate is reached, so you do not have to check manually every day.

- Consider forward-style transfers. Some providers allow you to lock in today's rate for a future transfer, protecting you from unfavorable movements.

- Diversify your providers. No single provider is consistently best across all currency corridors. Comparing options regularly is one of the best forex risk management habits a regular sender can build.

- Avoid airport and hotel exchange booths. These typically carry the highest markups of any option available to you.

Understanding the role of exchange rates in decision making means recognizing that timing, provider choice, and rate monitoring all have measurable financial consequences. This is not passive knowledge. It directly affects what lands in your recipient's account.

Pro Tip: If you send money on a recurring schedule, try staggering transfers over different days of the month rather than always sending on the same date. Exchange rates fluctuate daily, and even small timing adjustments can improve your average rate over time.

My take on the real cost hiding in plain sight

I've seen countless people obsess over transfer fees while completely ignoring exchange rate markups, and it's the single most expensive mistake regular senders make. A provider charging $0 in fees but applying a 3% rate markup on a $1,000 transfer is costing you $30 in invisible fees. That's often more than competitors charge in visible fees combined.

What I've learned from tracking the remittance space closely is that the providers offering the best net rates aren't always the biggest names. Fintech companies built for specific corridors frequently outperform legacy players on exchange rates precisely because their cost structure is leaner.

There's also a mindset shift worth making. Most people approach sending money like a transaction to complete quickly. Smart senders treat it as a financial decision that rewards patience and comparison. The essential trading factors that experienced currency traders use, including timing, benchmark awareness, and understanding what moves rates, translate directly to everyday remittances at a much smaller scale.

Technology is finally making transparency easier. Real-time rate aggregators now surface what used to take hours of research. The information exists. The senders who use it consistently come out ahead.

— Brahim

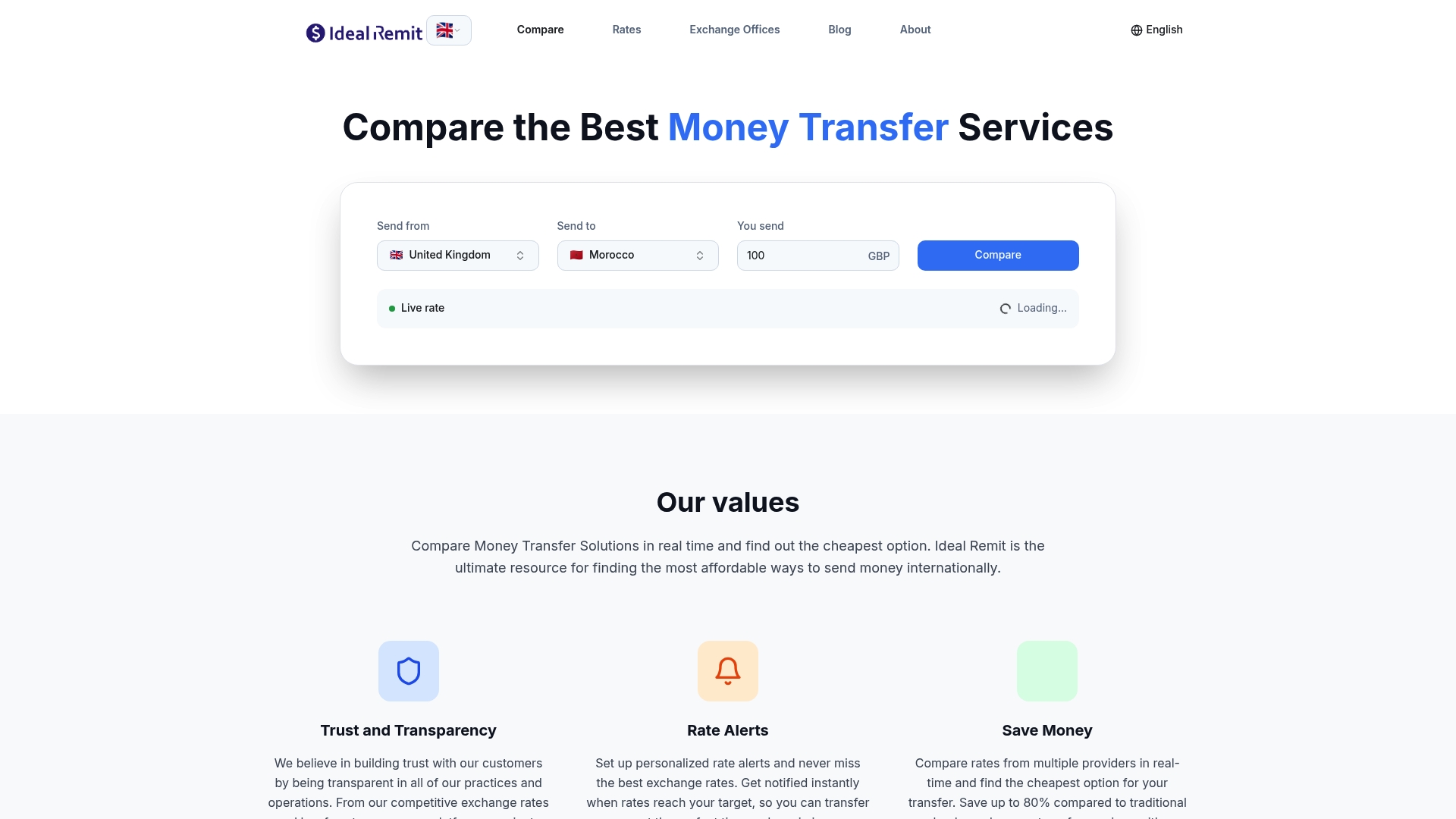

Find the best rate for your next transfer

Exchange rates and fees together determine the true cost of any international transfer. Idealremit exists to make that comparison fast and transparent.

With Idealremit, you can compare money transfer services side by side, seeing both fees and exchange rates in one view so you always know the actual amount your recipient will receive. The platform covers transfers to over 100 countries and includes trusted providers like Wise, Remitly, Western Union, and more. You can also set personalized rate alerts so you send at the right moment rather than guessing. Users who compare through Idealremit can save up to 80% compared to traditional bank transfers. Before your next transfer, check what the best rate available today actually looks like.

FAQ

What is the role of exchange rates in remittance?

Exchange rates determine how much of the destination currency a recipient receives after a money transfer. Even a small difference in the rate applied can significantly change the amount delivered, especially on larger or recurring transfers.

Why do money transfer providers offer different exchange rates?

Providers add their own markup to the mid-market rate to cover costs and generate profit. These markups vary based on business model, operating costs, and how each provider manages currency risk.

How do currency conversion fees affect the total cost of a transfer?

Currency conversion fees and FX margins together average around 6.35% of the transfer amount for low-income country corridors. This means the effective cost is often much higher than the advertised flat fee suggests.

Can exchange rates change between when I initiate and complete a transfer?

Yes. Some providers lock in your rate at the time you confirm the transfer, while others apply the rate at the moment the transaction processes. Always check which policy your provider uses before sending.

How can I get the best exchange rate when sending money abroad?

Compare the total recipient amount across multiple providers, not just fees. Use rate alerts to send when rates are favorable, and always benchmark against the current mid-market rate to gauge how large a provider's markup actually is.