TL;DR:

- Remittance delays often stem from incorrect beneficiary details, timing issues, compliance checks, and intermediary banks, with errors being the most preventable cause.

- To avoid delays, verify recipient information, send transfers early in the week, and choose providers with direct bank relationships in the destination country.

You sent money three days ago, and it still hasn’t arrived. No explanation, no updates, just silence. Understanding why remittance delays happen is not just about satisfying curiosity. It’s the first step toward doing something about it. The causes of remittance delays range from a single typo in a bank account number to regulatory screening that can hold funds for weeks. This article breaks down every major factor affecting money transfer speed, and more importantly, tells you what you can actually do to avoid them next time.

Table of Contents

- Key takeaways

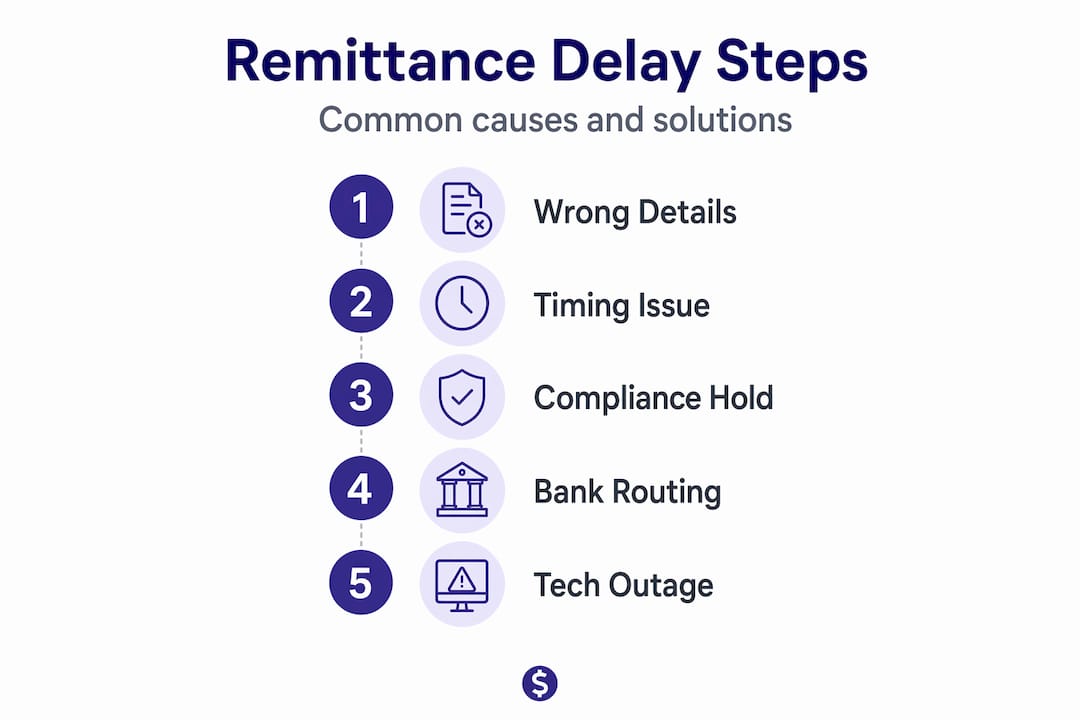

- Why remittance delays happen: the payment details problem

- Timing factors that slow down your transfer

- Compliance checks and regulatory hurdles

- Correspondent banks and currency conversion

- Technical and infrastructure factors

- My take on where the real responsibility lies

- Send smarter with Idealremit

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Errors trigger manual queues | A single wrong digit in an IBAN or SWIFT code pulls your transfer into a correction queue that can add days. |

| Timing kills speed | Sending after a bank’s daily cut-off or before a holiday weekend can silently add 2 to 3 business days. |

| Compliance is by design | AML and sanctions screening are built into the system on purpose and cannot be skipped, only prepared for. |

| Intermediary banks multiply delays | Each correspondent bank in the chain runs its own checks and operates on its own schedule, compounding wait times. |

| Better data means faster transfers | Clean, accurate beneficiary details and pre-prepared documents are the most effective way to cut processing time. |

Why remittance delays happen: the payment details problem

The single most preventable cause of delayed remittances is also the most overlooked: bad data. When you enter a recipient’s name, bank account number, SWIFT/BIC code, or IBAN, even one character out of place sends your transfer into a manual correction queue. Incorrect or missing beneficiary details are the leading cause of remittance delays, pushing processing well beyond the standard 1 to 3 business day window.

Here is what commonly goes wrong:

- A typo in the recipient’s name that does not match the bank’s records

- A SWIFT code that belongs to a different branch or country

- An IBAN with a missing digit or incorrect country prefix

- An account number that is valid but belongs to someone else entirely

Each of these errors forces a human being to step in and investigate. That process alone can take 24 to 72 additional hours, and if the issue requires contacting the recipient’s bank, it can stretch even further. Building a repeatable process for verifying beneficiary information before every transfer is the cleanest solution available.

Pro Tip: Before confirming any transfer, read every field back against the recipient’s bank statement or a screenshot they have sent you. Pay special attention to the IBAN and the exact legal name on the account.

Timing factors that slow down your transfer

Most people assume a transfer starts moving the moment they hit “send.” It does not. Banks operate on daily cut-off times, and if your transfer is submitted even minutes after that threshold, it joins the next day’s batch. That one missed window can cost you an entire business day before your money moves at all.

The timing problem compounds across borders because the sender’s bank, any intermediary bank, and the recipient’s bank each operate on their own schedules in different time zones. Gaps in RTGS operating hours across jurisdictions mean that some country pairs experience overlapping operating windows of fewer than 4 hours per day. When your transfer misses that narrow window, it waits until the next one.

Weekends and public holidays make this worse in ways that are easy to underestimate. Consider what can happen on a Friday afternoon transfer:

- You send money Friday at 4:00 PM, just after your bank’s 3:30 PM cut-off.

- Your bank queues it for Monday processing.

- Monday is a public holiday in the recipient’s country.

- The recipient’s bank processes it Tuesday.

- Currency conversion adds another processing step on Tuesday afternoon.

- The money arrives Wednesday, five days after you sent it on a Friday.

No one did anything wrong. The system simply ran into its own calendar. Understanding this timing reality is one of the simplest ways to manage expectations and, when possible, schedule transfers earlier in the week.

Compliance checks and regulatory hurdles

Compliance screening is not a bank being slow. It is a legally mandated process, and some delay is intentionally built into global financial systems to manage credit risk and prevent money laundering. Automated systems scan every international transfer against sanctions lists, watchlists, and AML rules. When a transaction triggers a flag, a human compliance officer reviews it manually.

What causes a flag? Several things:

- Transfers above certain thresholds, even round numbers like $10,000

- Payments to countries under heightened regulatory scrutiny

- Inconsistent information between the sender’s profile and the transfer details

- A payment purpose that is vague or missing

“Delays can extend from days to weeks depending on document exchange and correspondent bank workflows.” Source: RBC Companies

Country-specific regulatory changes also create sudden friction. Nigeria’s Naira-only remittance rule is a real-world example: Nigeria’s Naira-only rule forces providers to manually match foreign currency, adding hours to each transaction or triggering partial settlements. Rules like this can change with little notice, and senders using corridors in affected regions often have no idea why their transfer suddenly takes twice as long.

Pro Tip: When sending large amounts or to high-scrutiny corridors, include a clear payment purpose in your transfer notes. “Family support” or “invoice payment ref. 1042” moves through screening faster than a blank field.

Correspondent banks and currency conversion

When your bank does not have a direct relationship with the recipient’s bank, it routes your transfer through one or more correspondent banks. Each one of those intermediaries performs independent compliance checks and operates on its own cut-off schedule. Your transfer is not one journey. It is a relay race with multiple handoffs, and each handoff takes time.

Currency conversion for less liquid currencies adds another layer. Exchanging dollars into euros is straightforward because both are highly liquid. Sending to a smaller market, like converting to West African CFA francs or Bangladeshi taka, requires matching buyers and sellers in a thinner market. That process can extend settlement time by a full business day.

Here is a comparison of how transfer structure affects speed and cost:

| Transfer type | Typical delivery time | Typical fees | Example corridor |

|---|---|---|---|

| Direct bank transfer | 1 to 2 business days | Low to moderate | USD to EUR |

| Single correspondent bank | 2 to 4 business days | Moderate | USD to GBP via intermediary |

| Multiple correspondent banks | 3 to 7 business days | Higher | USD to PKR or NGN |

| Fintech direct network | Same day to 24 hours | Low | USD to MXN via app |

The average cost of sending $200 internationally still sits around 6.36%, even with fintech competition. Much of that cost exists precisely because of the intermediary infrastructure involved. When you use a comparison tool to find a faster route, you are often finding a provider that has built direct relationships with local banks in the destination country, cutting both fees and transit time.

Pro Tip: For popular corridors like USA to Mexico, specialized providers often have direct bank partnerships that skip correspondent banks entirely. Always compare before sending.

Technical and infrastructure factors

Beyond human processes, the underlying technology used by many banks is itself a source of delay. A large share of cross-border payment infrastructure still runs on legacy batch processing systems that group transactions together and process them at set intervals rather than in real time. Your transfer may simply sit in a queue waiting for the next batch window to open.

System maintenance windows, unplanned outages, and high transaction volumes during peak periods also cause temporary delays that are invisible to senders. ISO 20022, the new global messaging standard for financial transactions, is being adopted by major networks to address many of these interoperability problems. However, most transfer delays happen after the SWIFT messaging step is complete. The real bottleneck is in the final crediting to the recipient’s account, which depends entirely on the receiving bank’s own systems and processes.

| Delay factor | Cause | Typical impact |

|---|---|---|

| Batch processing | Transactions grouped, not real-time | 4 to 24 hours added |

| System maintenance | Scheduled downtime | 2 to 12 hours added |

| Legacy interoperability | Incompatible platforms | Varies by corridor |

| Last-mile crediting | Receiving bank processing speed | 12 to 48 hours added |

The shift toward ISO 20022 and real-time gross settlement systems is gradually reducing these friction points, but the transition is uneven across countries and banks. For now, the best protection a sender has is choosing a provider that has already built around these limitations.

My take on where the real responsibility lies

I’ve spent years watching people blame their bank for delays that had nothing to do with the bank. And honestly, that frustration is understandable. But in my experience, the picture is more complicated than “banks are slow.”

What I’ve found is that most preventable delays trace back to the sender. Not because senders are careless, but because no one has ever explained to them that a transfer is not a single transaction. It’s a chain of dependencies, and the weakest link is almost always the accuracy of the data at the start.

The uncomfortable truth I’ve learned is this: compliance delays are not the bank being difficult. They are a feature, not a bug. When a system holds a $5,000 transfer for review, it may be doing exactly what it is designed to do to protect both you and the financial system. Getting angry at that process helps no one. What does help is having your payment documents ready before compliance asks for them, because that alone can cut a multi-day review down to hours.

I also think people underuse the MT-103 document. If your transfer has been stuck for more than 48 hours, you can request an MT-103 from your sending bank. It is the formal SWIFT confirmation that your payment actually left the bank and is in the system. That document shifts the conversation from “we’re looking into it” to a traceable event with a paper trail.

The senders who have the smoothest experiences are not lucky. They follow a process. Accurate recipient data, mid-week timing, clear payment purpose, and a provider that has built around correspondent bank limitations. That combination eliminates most delays before they start.

— Brahim

Send smarter with Idealremit

If a delayed transfer has ever cost you a late fee, a missed bill, or an anxious phone call from family abroad, you already know the stakes. Idealremit was built specifically to cut through the confusion.

Idealremit compares real-time rates, fees, and delivery speeds across dozens of trusted providers, including options that bypass slow correspondent bank networks entirely. Whether you’re sending to Morocco, Mexico, the Philippines, or anywhere across Africa and Asia, you can compare transfer services and see exactly how long each option takes before you commit. Use Idealremit to find the fastest route for your corridor, set up rate alerts, and stop wondering why your money hasn’t arrived. Smarter transfers start with better information.

FAQ

What are the most common reasons for remittance delays?

The most common reasons include incorrect beneficiary details, compliance screening flags, transfers submitted after bank cut-off times, and delays caused by correspondent banks in the payment chain. Each factor adds time independently, and they often combine.

How long do remittance delays typically last?

Most delays resolve within 1 to 5 business days, but compliance-related holds requiring document verification can extend to 2 to 4 weeks depending on the corridor and the information provided.

What is an MT-103 and how does it help?

An MT-103 is a formal SWIFT message confirming that your payment has been released by the sending bank. You can request it from your bank to officially trace a stuck transfer and identify where in the chain the delay is occurring.

How can I avoid remittance delays on my next transfer?

Send early in the week, verify every digit of the recipient’s bank details, include a clear payment purpose, and use a provider with direct banking relationships in the destination country. These steps address the most frequent causes of delays.

Why does currency conversion slow down international transfers?

Converting into less commonly traded currencies requires matching buyers and sellers in thinner markets, which takes more time than exchanging major currency pairs. This process can add a full business day to settlement, particularly for corridors involving African or South Asian currencies.

Recommended

- How remittance aggregators simplify global money transfers - IdealRemit Blog

- Mobile money for global transfers: save more, send smarter - IdealRemit Blog

- Top 6 Ways to Send Money from USA to Mexico 2026 - IdealRemit Blog

- International transfer security checklist: safe and affordable - IdealRemit Blog