TL;DR:

- Remittances are the main financial link between migration and economic development, supporting households' immediate needs and long-term wealth building. They account for over $905 billion in 2024 and are essential in fragile states, funding vital services and investments. Digital platforms are improving transfer efficiency, but inclusion remains vital for reaching unbanked and vulnerable migrants.

Remittance is defined as money or goods sent by migrants to family members in their home countries, forming one of the most direct financial connections between migration and economic development. Global remittance flows exceeded $905 billion in 2024, making these transfers larger than foreign direct investment in many developing nations. For families in Morocco, Bangladesh, the Philippines, and across sub-Saharan Africa, remittances are not a supplement to income. They are the income. Understanding the role of remittance in migration means understanding how millions of families actually survive, invest, and build futures across borders.

How do remittances support local economies and household consumption?

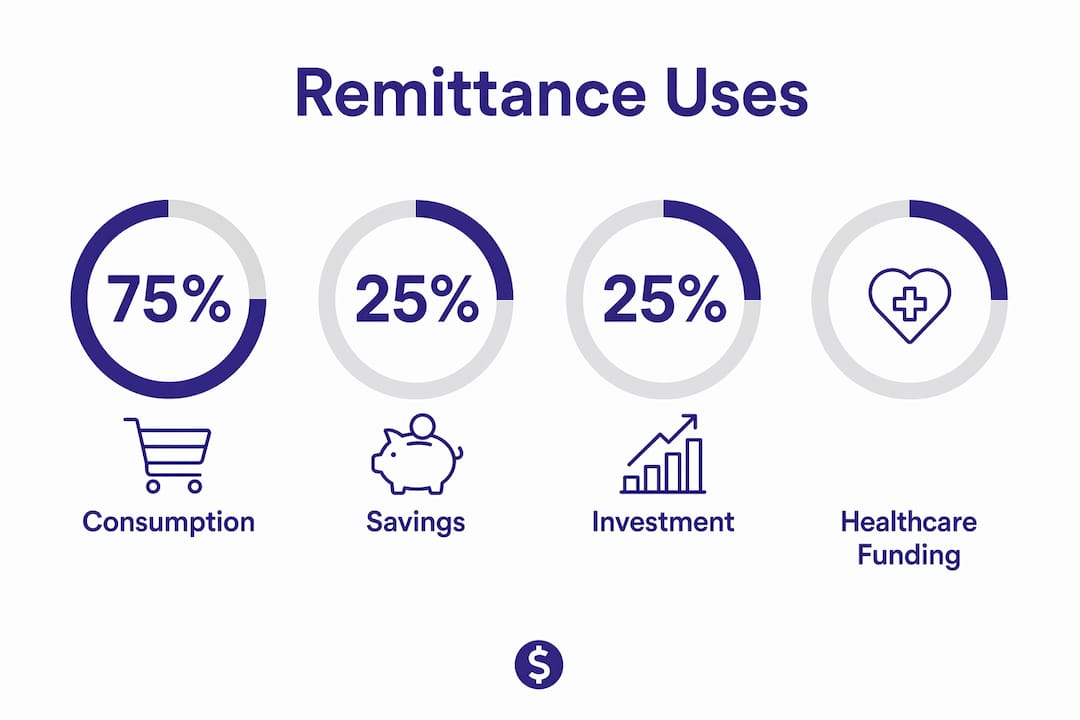

Remittances function as direct economic injections into communities that often lack other reliable income sources. Around 75% of remittances are spent immediately on food, rent, utilities, and basic services. That spending hits local GDP within the same quarter the money arrives, making remittances one of the fastest-acting forms of external finance available to developing economies.

The scale in fragile states is particularly striking. Remittances provide up to 50% of total external development finance in fragile contexts, with flows exceeding $134 billion in 2023. That means in countries affected by conflict, climate shocks, or institutional collapse, migrant families are effectively funding public welfare from abroad. No government program or aid package moves that fast or reaches that many households.

The economic ripple effect extends beyond the receiving family. When a household in rural Senegal pays rent, buys groceries, or hires a local repair worker, that money circulates through the local economy. Shopkeepers, landlords, and service providers all benefit. Over 60 countries receive remittances worth more than 5% of their GDP, which shows just how structurally embedded these flows have become.

Key consumption categories funded by remittances include:

- Food and groceries: The most immediate use, keeping families fed between irregular income cycles.

- Housing costs: Rent payments and utility bills that would otherwise go unpaid.

- Healthcare access: Covering medical visits, prescriptions, and emergency care.

- School fees: Keeping children enrolled when local wages fall short.

Beyond consumption: how remittances build long-term wealth

Not all remittance money disappears into daily expenses. About 25% of remittances globally go toward savings, business investments, or property acquisition. That share represents a meaningful shift from survival spending to wealth creation, and it compounds over time.

Healthcare investment is one of the clearest examples of this long-term impact. A 2025 study of remittance-dependent households in Bangladesh found that recipients increase healthcare spending by $2,000-$2,300 annually. That is not just better health outcomes for one family. It reduces long-term dependency on strained public health systems and builds human capital across a generation.

Education follows a similar pattern. Families receiving remittances show higher school attendance rates and spend more on tutoring, uniforms, and materials. Children in these households are more likely to complete secondary school and pursue higher education. The migrant working abroad is, in effect, funding the next generation's economic mobility.

Business creation is the third major channel. Remittance-receiving households start small enterprises at higher rates than their neighbors. A family in Mexico or Nigeria that receives steady transfers can accumulate enough capital to open a shop, buy farming equipment, or fund a trade apprenticeship. These businesses then hire locally, creating jobs that did not exist before.

- Savings accumulation: Families build emergency reserves and long-term capital buffers.

- Property investment: Land and home purchases that create generational wealth.

- Business startups: Small enterprises funded by remittance capital that employ local workers.

- Education investment: Higher school completion rates and access to post-secondary training.

- Healthcare spending: Preventive and emergency care that reduces long-term public health costs.

Pro Tip: If you send money home regularly, consider discussing a simple savings plan with your family. Even setting aside 10% of each transfer into a dedicated account can fund a business or property purchase within a few years.

What are the social and cultural dimensions of remittance flows?

Remittances are not purely financial decisions. They are socially embedded practices shaped by kinship obligations, gender roles, and what sociologists call the moral economy of the family. A migrant does not send money because a spreadsheet says it makes sense. They send money because their mother needs it, because a sibling is getting married, or because not sending would carry social consequences back home.

Gender shapes remittance behavior in ways that are often overlooked. Women migrants tend to send a higher proportion of their earnings home than men, even when earning less overall. They also direct funds more consistently toward children's education and healthcare. Men are more likely to fund construction projects or business investments. These patterns are not universal, but they appear consistently across corridors from Latin America to Southeast Asia.

"Remittances are not just transfers of money. They are transfers of obligation, identity, and belonging across borders." — Migration Policy Institute

The concept of non-financial remittances adds another layer. Highly skilled diaspora members contribute professional time and expertise that carry measurable economic value. A Ghanaian doctor advising a rural clinic remotely, or a Moroccan engineer reviewing infrastructure plans for a hometown project, provides services that would otherwise cost institutions real money. These contributions rarely appear in official remittance statistics, but their impact is real and growing.

What are the risks of remittance dependency?

Remittance dependency creates genuine economic vulnerabilities when it goes unmanaged. Excessive reliance on remittances can reduce local labor supply, because households with steady foreign income have less incentive to seek local employment. Over time, this weakens the domestic workforce and can slow the development of local industries.

Currency appreciation is a related risk. When large volumes of foreign currency flow into a small economy, the local currency strengthens. That sounds positive, but it makes exports more expensive on global markets, hurting farmers, manufacturers, and anyone who sells goods abroad. Countries like El Salvador and Tajikistan, where remittances represent a large share of GDP, have experienced this tension directly.

Transfer costs remain a persistent barrier. High fees and inconsistent regulation limit how much of each transfer actually reaches the recipient family. Fintech innovations have improved remittance affordability and security, but structural barriers like digital infrastructure gaps and regulatory inconsistency still hold back progress in many corridors. Understanding why remittance delays happen can help you avoid losing money to avoidable friction in the transfer process.

| Risk | Impact | Mitigation |

|---|---|---|

| Labor supply reduction | Fewer workers seek local jobs | Government employment programs |

| Currency appreciation | Exports become less competitive | Central bank intervention |

| High transfer fees | Less money reaches families | Use fintech or comparison platforms |

| Economic dependency | Vulnerability to migrant income shocks | Diversify household income sources |

Pro Tip: Compare transfer fees before every send. A 1% difference in fees on a $500 transfer saves $5 each time. Over 12 transfers a year, that is $60 back in your family's pocket.

How is fintech changing the way migrants send money home?

Digital platforms and mobile money services have fundamentally changed the remittance experience for migrants and their families. Services like Wise, Remitly, and Western Union's digital channels now offer faster transfers at lower costs than traditional bank wires. Mobile money adoption has been especially transformative in sub-Saharan Africa, where platforms like M-Pesa allow recipients to receive funds without a bank account.

The reality for many migrants is more complex, though. Many migrants rely on a mix of mobile money wallets and informal cash networks because formal banking excludes them. Undocumented migrants, those without credit histories, and workers in informal economies often cannot open bank accounts in their host countries. This creates a hidden remittance ecosystem that is harder to track and often more expensive per transaction.

Regional cooperation is making a difference in corridors where it exists. Southern Africa has seen improvements in remittance flows where fintech companies have partnered with local mobile operators and regulators have created clearer licensing frameworks. The lesson is that technology alone does not solve the problem. Inclusive regulation and cross-border cooperation are what allow fintech to reach the migrants who need it most.

Key developments shaping digital remittances in 2026:

- Mobile wallets: Recipients in rural areas receive funds without visiting a bank branch.

- Real-time transfers: Same-day delivery is now standard on major digital corridors.

- Rate transparency: Apps show the full cost of a transfer before you commit.

- Regulatory sandboxes: Some governments allow fintech pilots that test new transfer models safely.

Key Takeaways

Remittances are the single most direct financial link between migration and economic development, and managing them well requires both the right tools and a clear understanding of their social weight.

| Point | Details |

|---|---|

| Consumption drives immediate impact | 75% of remittances fund food, rent, and utilities, boosting local GDP within the same quarter. |

| Investment builds long-term wealth | 25% of global remittances go toward savings, property, and business startups that create jobs. |

| Social norms shape sending behavior | Kinship obligations and gender roles influence how much migrants send and where the money goes. |

| Dependency carries real risks | Unmanaged reliance on remittances can weaken local labor markets and hurt export competitiveness. |

| Fintech lowers costs but needs inclusion | Digital platforms reduce fees, but undocumented and unbanked migrants still face access barriers. |

Remittances are more than money transfers

Working with migrant communities over the years has shown me one thing clearly: the economic data on remittances tells only half the story. The other half is the weight a person carries when they wire money home. The guilt of not sending enough. The pride of funding a sibling's university degree. The quiet anxiety of watching exchange rates the way a farmer watches weather.

What I have found is that most migrants are remarkably disciplined senders. They cut their own expenses before they cut what they send home. That discipline deserves better infrastructure than a bank wire with a 5% fee and a three-day delay. The role of financial inclusion in remittance is not a policy abstraction. It is the difference between a family receiving $475 or $500 from the same transfer.

The risk I see most often is not dependency. It is the absence of a plan. Families receive money and spend it well on immediate needs, but nobody sits down to talk about what happens if the migrant loses their job, gets sick, or decides to return. Financial literacy at the household level, combined with accessible savings products in receiving countries, would do more for long-term development than almost any policy intervention I can name.

Technology is genuinely improving things. But the migrants who need the most help, those who are undocumented, unbanked, or sending to fragile states, are still the least served by the platforms getting the most attention. Inclusion has to be built into the design, not added as an afterthought.

— Brahim

How Idealremit helps you send more and spend less

Every dollar lost to fees is a dollar that does not reach your family. Idealremit compares the real costs of top money transfer services, including Western Union, MoneyGram, Remitly, and Wise, so you see exactly what your recipient gets before you send.

Idealremit tracks live exchange rates, lets you set personalized rate alerts, and calculates your potential savings across providers. Transfers are supported to over 100 countries, with strong coverage across Africa, Asia, Europe, and the Americas. Compare the cheapest rates available right now and make sure every transfer goes as far as it possibly can. For added confidence, check Idealremit's guidance on trusted transfer providers before you send.

FAQ

What is the role of remittance in migration?

Remittances are funds sent by migrants to family members in their home countries, serving as a direct financial link between migration and economic development. They fund household consumption, healthcare, education, and business investment in receiving communities.

How much do global remittances total?

Global remittance flows exceeded $905 billion in 2024, making them one of the largest sources of external finance for developing countries. In over 60 countries, remittances account for more than 5% of GDP.

What percentage of remittances goes to savings and investment?

About 25% of global remittances are directed toward savings, business investments, or property purchases. The remaining 75% funds immediate household consumption like food, rent, and utilities.

Do remittances have social as well as economic effects?

Remittances are shaped by kinship obligations, gender roles, and cultural norms, not just economic logic. Non-financial remittances, such as diaspora professional expertise, also carry measurable economic value for receiving communities.

How can migrants reduce the cost of sending remittances?

Using digital platforms and comparison tools like Idealremit helps migrants find the lowest fees and best exchange rates across providers such as Wise, Remitly, and Western Union. Checking rates before every transfer prevents unnecessary losses to fees.