TL;DR:

- Cost-effective remittance involves using services that reduce both visible fees and hidden exchange rate markups to maximize recipient funds. Digital providers like Wise and Remitly save senders over $340 annually compared to banks by offering lower costs and better transparency. Choosing regulated, corridor-specific providers ensures safer, more affordable transfers that support economic growth and financial inclusion.

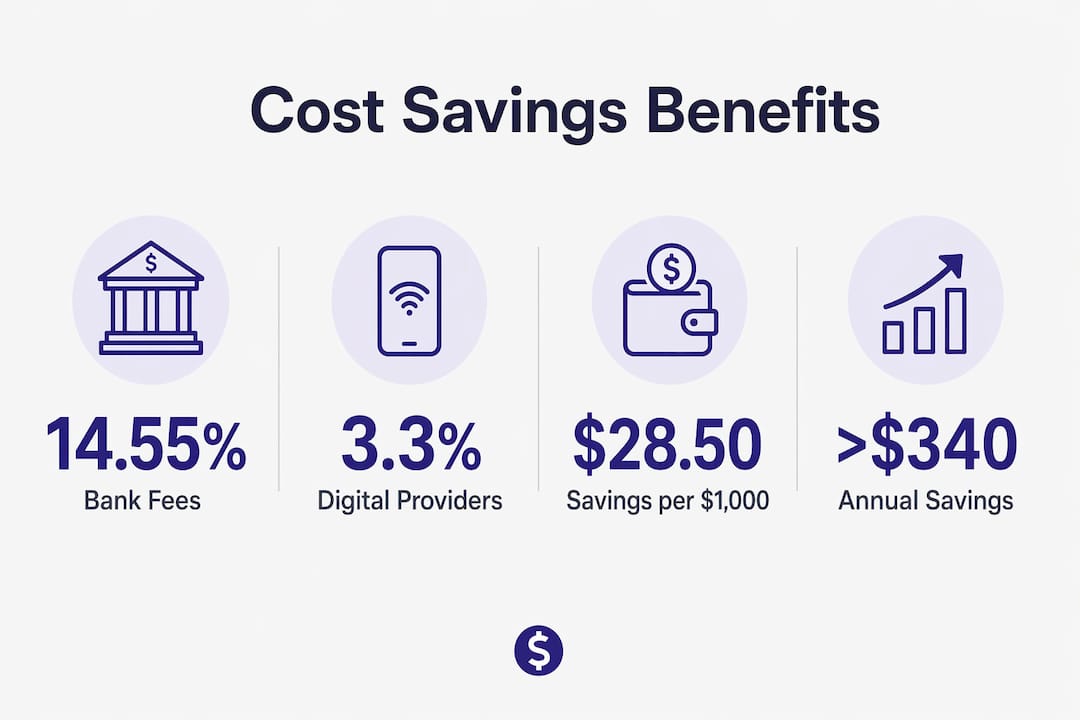

Cost-effective remittance is defined as sending money internationally using services that minimize total transfer costs, including both visible fees and hidden exchange rate markups, to maximize the amount recipients actually receive. Specialist digital providers like Wise, Remitly, and OFX have made this goal achievable for millions of senders. Specialist providers average $24.33 per $1,000 transfer versus $34.91 for traditional banks, saving senders roughly $28.50 per transfer. For anyone sending money monthly, that compounds to over $340 in annual savings. Choosing low-cost remittance services is not just a financial preference. It is a decision with real consequences for the families and communities on the receiving end.

Why choose cost-effective remittance over traditional banks

The industry term for what most people call "cheap" or "affordable" money transfers is low-cost remittance, and it covers the full picture of what a transfer actually costs you. Most senders focus only on the transfer fee listed at checkout. That is a mistake. Total transfer cost includes both the visible fee and the exchange rate markup, which is often hidden but can exceed the transfer fee itself.

Here is how the cost structure breaks down across provider types:

| Cost component | Traditional banks | Specialist providers (Wise, Remitly, OFX) |

|---|---|---|

| Average transfer cost | 14.55% | 3.3% |

| Exchange rate markup | Often 2–4% above mid-market | Near mid-market or 0% |

| Fixed transfer fee | $25–$50 per transfer | $0–$5 per transfer |

| Hidden intermediary fees | Common | Rare |

Banks charge an average of 14.55% per transfer versus 3.3% for digital specialists. That gap is not a rounding error. It represents hundreds of dollars a year for regular senders.

Exchange rate markups deserve special attention because they are rarely disclosed upfront. A 1% markup on a $1,000 transfer costs you $10 before any fee is charged. On a $5,000 transfer with a 3% markup, you lose $150 before the transaction even processes. Banks routinely apply markups in this range without labeling them as fees.

Pro Tip: Always compare the mid-market exchange rate on Google or XE.com against the rate your provider offers. The difference is your hidden markup cost. If a provider shows a "zero fee" transfer but offers a rate 2% below mid-market, you are still paying.

How transfer corridor affects what you actually pay

Not all remittance routes cost the same, and the difference can be dramatic. The global average cost of sending $200 internationally dropped to approximately 6.0% in Q1 2026, but that average masks enormous variation. High-volume corridors like US to India or US to Mexico benefit from intense provider competition and digital infrastructure, pushing costs below 3%. Lower-volume corridors, particularly those serving Sub-Saharan Africa, regularly exceed 8–10%.

Several factors drive this variation:

- Corridor volume: More senders on a route means more providers competing, which drives fees down.

- Digital adoption: Countries with strong mobile banking infrastructure receive transfers cheaper and faster.

- Regulatory environment: Strict compliance requirements in some markets add operational costs that providers pass on to senders.

- Bank de-risking: The number of active correspondent banks fell over 20% between 2011 and 2019, reducing formal banking access in certain corridors and pushing costs up.

- Currency liquidity: Exotic or less-traded currencies cost more to convert, adding to the total expense.

Bank de-risking is particularly damaging for senders in underserved corridors. When correspondent banking relationships disappear, formal transfer options shrink. Senders then face a choice between expensive remaining formal channels and informal networks that carry real security risks. Digital innovation offers a path out of this trap by bypassing traditional correspondent banking entirely.

Understanding your specific corridor is one of the most underrated steps in choosing budget remittance options. A provider that is cheapest for US to Philippines transfers may not be the best choice for US to Nigeria. Corridor-specific comparison tools give you the accurate picture.

What are the real benefits of affordable money transfer?

The benefits of affordable money transfer extend well beyond what stays in your wallet. When more money reaches recipients, the downstream effects are measurable and significant.

Families receiving remittances in developing economies typically spend the additional funds on healthcare, education, and nutrition. Savings from cost-effective remittances boost recipient families' disposable income and drive local economic growth. This is not a marginal effect. Remittances to low and middle-income countries totaled over $650 billion in recent years, meaning even a 1% reduction in average fees redirects billions of dollars from financial intermediaries to actual families.

"Each dollar saved on remittance fees translates to real, tangible benefits in receiving communities, improving access to essentials and stimulating local economies." — Economic impact of cross-border payments

Security is another underappreciated advantage of using regulated, low-cost providers. When formal channels are too expensive, senders turn to informal networks, hawala systems, or cash couriers. These options carry fraud risk, no recourse if something goes wrong, and potential legal exposure. Regulated specialist providers like Remitly and Wise operate under financial authority licenses, offer transaction tracking, and provide customer support if a transfer fails. The advantages of cheap remittance through trusted providers include both lower cost and stronger consumer protection, a combination informal channels cannot offer.

There is also a financial inclusion dimension. When affordable options exist, more people participate in the formal financial system. Recipients who receive regular transfers through digital platforms often gain access to savings accounts, credit products, and insurance for the first time.

How to choose budget remittance options that are safe and reliable

Choosing the right provider in 2026 requires looking at total cost, speed, reliability, and security together. Here is a practical framework:

- Compare total cost, not just fees. Use a fee calculator that shows the exchange rate alongside the transfer fee. Idealremit's comparison tool displays both components side by side across multiple providers.

- Use bank-to-bank transfers. Card funding adds 1–2% in surcharges on top of the base fee. Funding your transfer directly from a bank account avoids this entirely.

- Check your specific corridor. Run a comparison for your exact sending and receiving countries. A provider ranked cheapest overall may not win on your route.

- Leverage first-transfer promotions strategically. First-time promotions can eliminate fees on initial transfers. Savvy senders use multiple providers to capture these offers while maintaining a primary trusted provider for reliability.

- Set rate alerts. Exchange rates fluctuate daily. Platforms like Idealremit let you set alerts so you transfer when rates are most favorable.

- Verify regulatory status. Confirm your provider holds a license from a recognized authority such as FinCEN in the US, the FCA in the UK, or ASIC in Australia. Licensed providers are audited and accountable.

Pro Tip: Avoid cash pickup options unless the recipient has no bank account. Cash pickup typically costs 1–3% more than bank deposit delivery and adds risk at the collection point.

A practical comparison of popular provider types helps clarify the trade-offs:

| Provider type | Average cost | Speed | Best for |

|---|---|---|---|

| Traditional bank wire | 14.55% | 3–5 business days | Large, infrequent transfers |

| Specialist digital (Wise, Remitly, OFX) | 3.3% | Minutes to 2 days | Regular, cost-sensitive senders |

| Mobile wallet services | 2–5% | Instant to 1 day | Recipients without bank accounts |

| Cash transfer services | 5–10% | Instant | Emergency cash pickup |

For most regular senders, specialist digital providers deliver the best combination of low cost, speed, and security. The key is comparing them on your specific corridor rather than relying on general rankings.

Key takeaways

Choosing cost-effective remittance means comparing total transfer cost, including fees and exchange rate markups, across specialist digital providers to maximize the money recipients actually receive.

| Point | Details |

|---|---|

| Total cost beats listed fees | Always factor in exchange rate markup, which can exceed the transfer fee itself. |

| Corridor determines your rate | High-volume routes like US to India cost far less than underserved Sub-Saharan corridors. |

| Specialists beat banks consistently | Digital providers average 3.3% versus banks at 14.55%, saving over $340 annually for monthly senders. |

| Security comes with savings | Regulated low-cost providers offer fraud protection and recourse that informal channels cannot match. |

| Funding method matters | Bank-to-bank transfers avoid card surcharges of 1–2%, reducing total cost further. |

The real cost of staying with your bank out of habit

I have spoken with hundreds of senders over the years who genuinely believed their bank was the safest option for international transfers. Safe, yes. Cheap, absolutely not. The data is unambiguous: banks extract an average of 14.55% from every transfer, while digital specialists charge 3.3%. That is not a small difference in service quality. It is a structural overcharge that costs families real money every single month.

What frustrates me most is that the information to make a better choice has never been more accessible. Fee calculators, rate alerts, and comparison platforms exist precisely to close this knowledge gap. Yet many senders still default to their bank because switching feels complicated or risky. It is neither. Providers like Wise and Remitly are regulated, insured, and used by tens of millions of people globally.

The fraud concern cuts the other way, too. Informal transfer networks, which senders turn to when formal options feel too expensive, carry far greater risk than any licensed digital provider. Choosing an affordable, regulated service is simultaneously the cheapest and the safest decision available. I would encourage every sender to spend 10 minutes on a comparison platform before their next transfer. The savings are real, and the families receiving the money will feel the difference.

— Brahim

Find the cheapest transfer for your corridor with Idealremit

Idealremit is built specifically for senders who want to stop overpaying. The platform aggregates real-time rates and fees from trusted providers including Wise, Remitly, Western Union, MoneyGram, and OFX, then displays total transfer cost so you see exactly what your recipient receives. You can compare transfer rates now across your specific corridor in seconds, set personalized rate alerts, and calculate potential savings against your current provider. Idealremit supports transfers to over 100 countries with transparent pricing and no hidden markups. For senders in the UK, the UK comparison tool offers the same real-time data tailored to GBP transfers. Stop guessing and start comparing.

FAQ

What does cost-effective remittance actually mean?

Cost-effective remittance means sending money abroad using a service that minimizes total transfer costs, including both the transfer fee and the exchange rate markup, so the recipient receives the maximum possible amount.

Why are specialist providers cheaper than banks for international transfers?

Banks charge an average of 14.55% per transfer versus 3.3% for digital specialists, because banks apply large exchange rate markups and fixed fees while specialist providers operate on thinner margins with higher transaction volumes.

How much can I save by switching from a bank to a specialist provider?

Switching saves approximately $28.50 per $1,000 transfer, which compounds to over $340 annually for senders who transfer monthly, based on Q1 2026 market data.

Why do some transfer corridors cost more than others?

Corridor costs depend on transaction volume, local digital infrastructure, regulatory complexity, and correspondent banking availability. High-volume routes like US to India benefit from competition and cost below 3%, while some Sub-Saharan corridors exceed 8–10%.

How do I avoid hidden fees when sending money abroad?

Compare the exchange rate your provider offers against the mid-market rate on Google or XE.com, fund transfers via bank account rather than card to avoid 1–2% surcharges, and use a comparison platform that displays total cost rather than just the listed transfer fee.