How remittance aggregators simplify global money transfers

TL;DR:

- Remittance aggregators connect multiple payment rails through a single platform, simplifying cross-border transfers. They automatically select the fastest, cheapest routes, reducing fees and operational complexity for users. This technology provides greater reach, convenience, and reliability for individuals sending money to multiple countries.

Sending money internationally can feel like solving a puzzle with too many pieces. You check one app for rates to the Philippines, a different platform for transfers to Mexico, and yet another service when your family in Morocco needs funds urgently. By the time you've compared fees, read the fine print, and figured out which payout method your recipient can actually use, you've spent an hour just trying to send a few hundred dollars. Remittance aggregators exist to cut through that chaos. This guide explains exactly what they are, how they work, and how you can use them to make smarter, cheaper, and faster transfers to any corner of the world.

Table of Contents

- What is a remittance aggregator?

- How remittance aggregators operate: Workflow and technology

- Key benefits and limitations for immigrants and expatriates

- Choosing the right remittance aggregator: What to look for

- The hidden edge: Why savvy users rely on aggregators for global remittance

- Explore top remittance aggregators and find your best fit

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Single interface advantage | Remittance aggregators streamline sending money abroad by providing one platform for multiple payment methods and countries. |

| Dynamic routing savings | They automatically choose the best rail for speed and cost, often helping you save money and deliver funds faster. |

| Compliance assurance | Aggregators handle compliance steps like KYC and AML, increasing both safety and reliability. |

| User-focused convenience | Frequent senders, especially immigrants, benefit most by avoiding manual comparisons and transfer hassles. |

What is a remittance aggregator?

Most people are familiar with individual money transfer services: you sign up, enter recipient details, and send funds through that company's specific network. A remittance aggregator is a fundamentally different model. Rather than relying on a single delivery network, it connects to many payment rails simultaneously.

Think of it like a flight aggregator. Instead of checking each airline's website separately to find the cheapest ticket, one platform pulls all the options together so you can compare and choose in seconds. A remittance aggregator does exactly that for money transfers, but instead of flights, it's routing your funds through bank rails, mobile wallets, card networks, and cash pickup networks.

According to Gate's financial glossary, a remittance aggregator is a multi-rail platform that provides a single interface for sending cross-border funds, routing delivery through various payment methods and handling compliance. That "single interface" part is the key. You don't see the complexity behind the scenes. You just see rates, speeds, and delivery options, and then you pick the one that works best.

Here's what happens when you initiate a transfer through a remittance aggregator:

- Funding: You deposit money via bank transfer, debit card, or another source.

- Compliance check: The platform verifies your identity and screens the transaction against anti-money laundering (AML) rules.

- Routing: The aggregator's engine selects the best available rail based on speed, cost, and corridor availability.

- FX conversion: Your funds are converted from the send currency to the receive currency at the quoted exchange rate.

- Payout: The recipient collects funds via bank deposit, mobile wallet, or cash pickup.

"A remittance aggregator handles the full transfer lifecycle in one place, from compliance to currency conversion to settlement, so the sender doesn't have to manage multiple services manually."

One important terminology note: in some financial contexts, "payment aggregator" refers to a merchant payments tool that bundles merchants under a master account. That's a different concept. When you see the phrase used in the remittance space, it specifically describes multi-rail routing for cross-border person-to-person or business-to-consumer transfers. Understanding that distinction helps you research the right providers. For guidance on secure money transfers and practical options by corridor, like ways to send money from USA to Mexico, aggregator-powered platforms are often your strongest starting point.

How remittance aggregators operate: Workflow and technology

Now that you know what remittance aggregators are, let's break down how they actually work. The technology underneath an aggregator is more sophisticated than it might look on the surface.

Modern remittance aggregators rely on API connections to embed multiple payment rails into a single platform. As described in ReadyRemit's developer documentation, aggregator-style cross-border services use APIs and embedded rails to integrate money movement, currency conversion, and settlement into one unified flow. This means a single platform can simultaneously maintain live connections to local bank networks in dozens of countries, mobile money operators like M-Pesa, global card schemes, and cash pickup networks.

Here's a step-by-step look at what happens during a real transfer:

- You initiate the transfer by entering the destination country, amount, and delivery method.

- The aggregator queries available rails in real time to find routes that can complete the transfer to that specific corridor.

- The routing engine evaluates each option based on speed, total fee, FX rate, and recipient eligibility.

- You see a ranked list of choices and select the one that fits your priorities.

- Compliance and KYC verification runs in the background, often instantly for returning users.

- Funds are moved through the selected rail, converted at the locked-in rate, and settled to the recipient.

The dynamic routing capability is what makes aggregators genuinely powerful. Gate's research confirms that dynamic routing based on fees, speed, and reachability is a defining feature of aggregator platforms. The system isn't manually managed. It adapts in real time to network availability and market conditions.

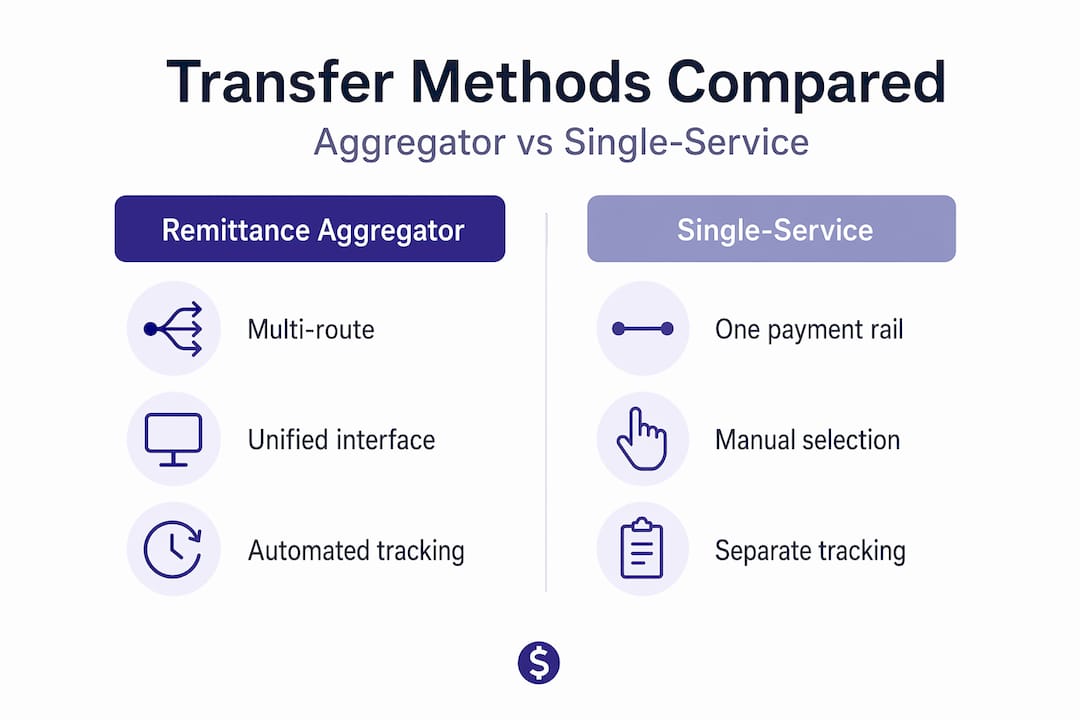

Comparison: Aggregator vs single-service transfer

| Feature | Remittance aggregator | Single-service transfer |

|---|---|---|

| Payment rail access | Multiple (bank, wallet, card, cash) | Usually one or two |

| Country coverage | Often 100+ destinations | Typically limited corridors |

| Rate optimization | Dynamic, route-by-route | Fixed markup per corridor |

| Compliance handling | Automated, platform-level | Varies by provider |

| User experience | One account, many options | Separate accounts per service |

The underlying currency exchange technology trends in fintech have driven down the cost of maintaining these multi-rail connections significantly, which is why aggregator platforms have become increasingly competitive with legacy transfer services.

Pro Tip: Always check how an aggregator quotes FX rates before committing. Some platforms show the mid-market rate prominently and add their margin transparently, while others embed a markup into the displayed rate without breaking it out separately. Knowing this difference helps you accurately compare the total cost of a transfer. Our remittance guides break down how to read rate quotes correctly for specific corridors.

Understanding remittance impacts on economies also helps explain why the technology has evolved so quickly. Trillions of dollars move across borders each year to support families and communities. The volume has attracted serious investment in routing technology and compliance infrastructure.

Key benefits and limitations for immigrants and expatriates

After examining the workflow and technology, it's important to understand what this means for real users who regularly send money home or across multiple countries.

The core advantages are real and significant. For an immigrant supporting family in two or three different countries, the traditional approach means maintaining separate accounts or relationships with different transfer services. Each service has its own app, its own identity verification process, and its own fee structure. Aggregators collapse all of that into one account. The aggregator value proposition is straightforward: one interface with automated rail selection versus a manual process for each country or bank.

Here's how the key benefits stack up for frequent senders:

- Speed: Aggregators often surface same-day or instant options that a single provider might not offer to a specific corridor.

- Cost savings: Routing to the cheapest available rail for each transfer can reduce fees significantly compared to using any single provider for all destinations.

- Reach: Coverage of 100+ countries through one account is standard for major aggregator-powered platforms.

- Convenience: One identity verification, one account history, one place to track all your transfers.

- Compliance protection: Regulated aggregators handle AML and KYC requirements systematically, which protects both you and your recipient.

Limitations are real too, and you should know them upfront. Not every aggregator covers every corridor equally well. As Gate's platform notes, routing effectiveness is corridor- and method-dependent. A platform might offer excellent rates to Nigeria via mobile wallet but limited options for cash pickup in rural Bangladesh. The FX markup structure can also vary widely, so a platform that looks cheap in fees might be recovering margin through the exchange rate.

Comparison: Aggregator vs corridor-specific service

| Factor | Aggregator platform | Corridor-specific service |

|---|---|---|

| Multi-country sending | Seamless, one account | Requires separate services |

| Rates to popular corridors | Competitive, route-optimized | Often specialized and sharp |

| Rates to minor corridors | Variable, sometimes limited | May not support at all |

| Payout method variety | Broad, multi-method | Can be narrow (e.g., bank only) |

| Compliance burden on user | Minimal, platform-managed | Varies, sometimes manual |

Practical things to check when evaluating any aggregator:

- Does it support your specific send and receive countries?

- What payout methods does it offer in the recipient's country (bank, mobile wallet, cash)?

- How is the FX rate quoted and is the margin disclosed transparently?

- What are the transfer limits, both minimum and maximum?

- How does customer support work if a transfer is delayed?

When you're ready to compare money transfer rates side by side, having these questions answered ahead of time makes the comparison meaningful. For U.S.-based senders, reviewing available money transfer services by destination corridor is the fastest way to shortlist platforms worth testing.

Choosing the right remittance aggregator: What to look for

With benefits and limitations clear, here's how you can select the right aggregator for your specific needs. The phrase "remittance aggregator" gets used loosely in the industry. As Gate explains, it describes multi-rail routing platforms as well as providers that bundle corridors behind one user experience. When you research options, map out exactly what the platform aggregates before assuming it covers your needs.

Here's a structured evaluation checklist:

- Verify corridor coverage. List every country you send to and confirm each one is supported. Don't assume. Check the platform's supported destinations page directly.

- Review payout method depth. Bank transfer may be available, but is mobile wallet delivery an option? Is cash pickup offered for recipients without bank accounts?

- Understand FX rate quoting. Ask or check whether rates are quoted at mid-market plus a disclosed fee or whether the margin is built invisibly into the rate. The total cost is what matters, not just the transfer fee.

- Check transfer limits. Some aggregators cap individual transfers or monthly volumes. If you send large amounts, these limits matter.

- Evaluate compliance and licensing. Is the platform licensed by a financial regulator in your country? This is a non-negotiable safety consideration.

- Read the speed disclosures. "Instant" often means instant to the aggregator's settlement partner, not necessarily to the recipient's account. Confirm realistic delivery times for your specific corridor.

- Test customer support before you need it. Send a message to customer support with a pre-transfer question and judge the response time and quality.

Pro Tip: Always run a small test transfer before sending a large sum through any new platform. Even if the pricing looks excellent on paper, a small test confirms that the delivery works as advertised for your specific corridor and payout method. This is especially important for less common destinations. Learning about remittance impacts for your recipient country can also help you understand which delivery options matter most to local recipients.

The hidden edge: Why savvy users rely on aggregators for global remittance

Let's step back and consider something that most guides miss entirely. The conversation about remittance aggregators almost always focuses on fees. Save money. Get better rates. That's true, but it's only part of the picture, and arguably not even the most important part for people who send money regularly.

The real value is operational relief. The aggregator's core advantage is one unified interface with automated rail selection, versus a manual process for every separate bank or transfer service. When you're sending money to three countries every month, that automation isn't just convenient. It removes a significant cognitive and logistical burden.

Think about what the old process actually looks like. You spend 20 minutes comparing rates across four apps, only to find that the cheapest option for Morocco has a payout delay that doesn't work this week, so you switch to your backup. Then you need to make sure your identity documents are current on each platform because different services have different reverification timelines. You track multiple transfers in multiple apps and hope nothing gets flagged for a manual review without notification.

Aggregators change that dynamic fundamentally. Compliance, routing, and tracking happen in one place. The system's regulatory work runs in the background. You're not responsible for knowing which rail is currently the fastest to Senegal or whether a particular mobile wallet is experiencing downtime in Indonesia. The platform manages that, and alerts you automatically.

For expatriates who support families in multiple countries simultaneously, this isn't a minor convenience. It's the difference between remittance being a stressful monthly chore and it becoming a routine, almost invisible process. That reliability compounds over time, especially when recipients are depending on consistent, on-time delivery.

We've observed that users who switch to aggregator-powered platforms for multi-corridor sending typically describe the biggest benefit not as cost savings but as peace of mind. When the technology works reliably, you stop worrying about transfers. That's worth a lot.

Explore top remittance aggregators and find your best fit

You now understand how remittance aggregators work, what to look for, and why they matter for multi-country senders. The logical next step is comparing what's actually available so you can find the platform that fits your specific corridors and sending habits.

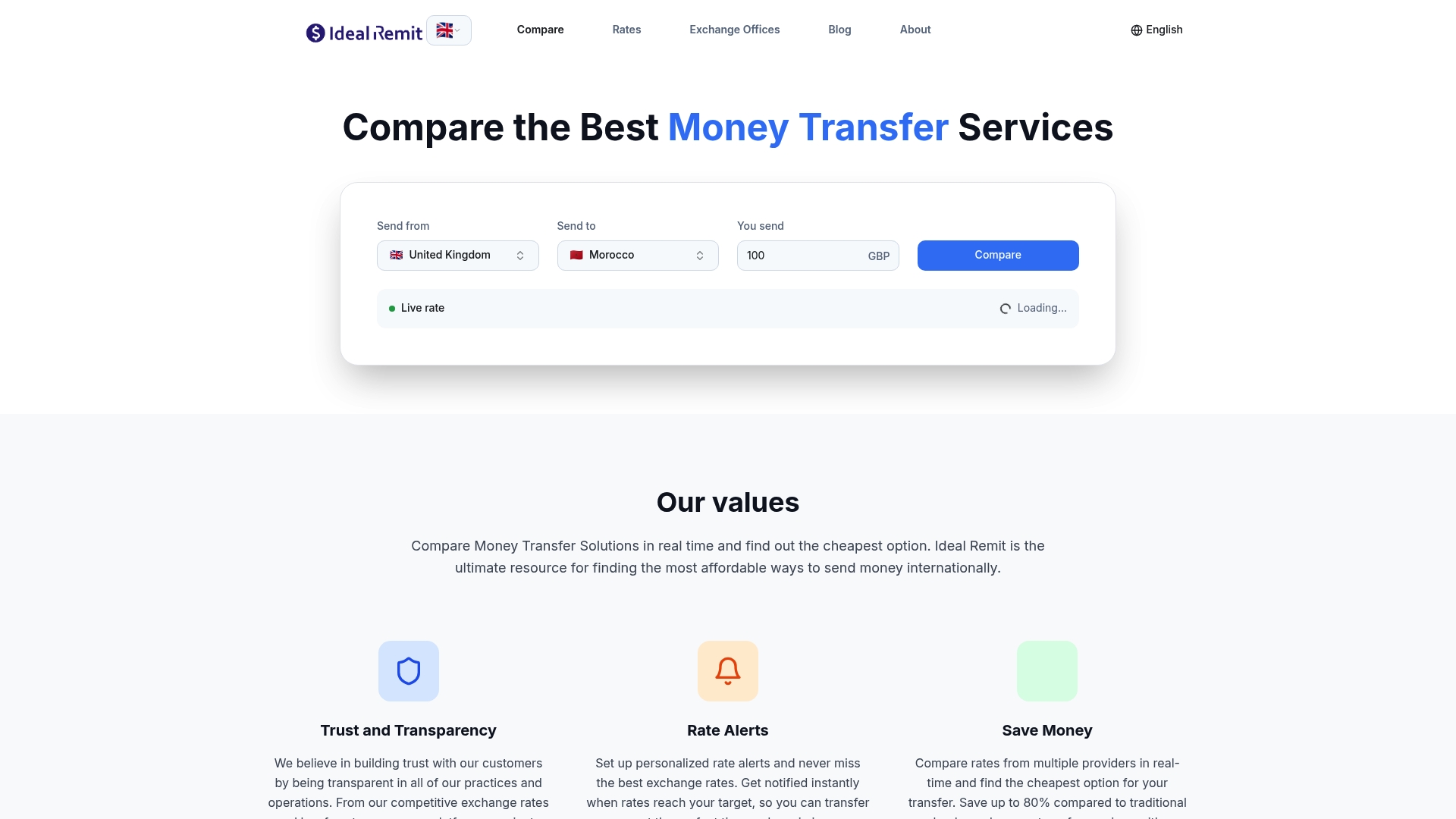

At Ideal Remit, we've built a platform specifically designed to make that comparison fast and accurate. Instead of visiting five different websites and manually calculating total costs, you can compare money transfer services across multiple aggregator-powered providers in one place. We surface real-time rates, total fees, and estimated delivery times so you can see exactly what each provider offers for your specific route. Visit the IdealRemit homepage to set up personalized rate alerts, track live exchange rates, and start saving on every transfer you make. Our platform covers over 100 countries and is built specifically for people who send money seriously.

Frequently asked questions

What makes a remittance aggregator different from a regular money transfer service?

Remittance aggregators provide a single interface for sending money through multiple payment rails and corridors, while regular services typically route through one or two networks and require you to compare options manually across platforms.

Can remittance aggregators save me money when sending funds abroad?

Yes, aggregators often optimize routing for lower fees and faster delivery, but the savings depend on the specific corridors and payment methods chosen since benefits vary by route.

Are remittance aggregators safe and reliable?

Aggregators generally handle compliance and integrate regulated payment rails as part of their core workflow, but you should always review each provider's regulatory licenses and security procedures before sending.

Do aggregators cover all countries and payment types?

Coverage depends entirely on the aggregator. Some support many corridors and diverse payout methods, others specialize in certain regions. Always verify your specific corridor and payout availability before initiating a transfer.

Recommended

Written by

Brahim Oubrik

Brahim Oubrik, a senior data engineer who experienced firsthand the challenges of sending money internationally. Living in France while supporting his family in Morocco, Brahim regularly needed to transfer funds across borders. Drawing on his background in data engineering, Brahim decided to solve this problem not just for himself, but for the millions of others navigating the same difficulties. He built Ideal Remit to bring clarity to the international money transfer market.