How Remittance Fuels Local Economies: Real Impacts

TL;DR:

- Remittances influence not only household stability but also broader community growth and economic resilience.

- Their impact varies based on household investment choices, financial access, and government policies, affecting exchange rates and competitiveness.

Many people assume that the money you send home simply covers groceries, rent, or school fees for the month. That assumption is only partly true. Research shows that remittances do far more than support families at the household level. Their macro and micro effects can determine whether entire communities flourish or struggle for years. This guide breaks down how remittances shape local economies, what happens to exchange rates and business competitiveness, and what you as a sender can do to make every dollar count even more for the people you love back home.

Table of Contents

- What remittance actually does for local households

- How remittance injects growth into the local economy

- Exchange rates, competitiveness, and the 'Dutch disease' debate

- Why household choices and financial access matter

- What most remittance guides miss—and what senders should actually do

- Send smarter: The next step for your family and community

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Household use matters | The way recipients use remittance money determines whether it fuels only short-term needs or long-term community growth. |

| Economic impact multiplies | Remittance inflows can boost local investment, job creation, and even education, with effects lasting for years. |

| Exchange rates complicate benefits | Positive impacts can sometimes come with downsides, like a stronger currency making local exports less competitive. |

| Policy and financial access shape outcomes | Strong local institutions and financial tools help remittance become a force for sustainable development, not just immediate aid. |

What remittance actually does for local households

Remittance, at its most basic, is money sent by a migrant worker or immigrant to family members in their home country. For millions of households across Africa, Asia, Latin America, and the Middle East, these transfers are the most reliable income source they have. But the story goes much deeper than just covering daily expenses.

One of the most important functions remittances play is consumption smoothing. This economic term means that families can maintain a stable standard of living even when local income fluctuates due to drought, job loss, or economic downturns. A farmer in Morocco who loses a harvest does not have to pull children out of school if a family member in France or Spain is sending money regularly. That stability is not just emotional comfort. It keeps children in classrooms and keeps local businesses running because families can still spend.

Beyond survival, remittances increasingly fund real investment. Research confirms that remittances improve livelihoods through mechanisms like consumption smoothing, better creditworthiness, and investment in human capital and small enterprises. When a family is known to receive regular transfers, local lenders are more willing to extend credit because that household is seen as lower risk. That creditworthiness opens doors to small business loans, home improvement financing, and agricultural inputs.

Main household uses of remittances:

- Paying for food, utilities, and daily living costs

- Funding school fees, uniforms, and tutoring

- Covering medical bills and emergency healthcare

- Repairing or building homes

- Launching or expanding small businesses

- Saving for future needs through cooperatives or savings groups

"Remittances can improve receiving-household livelihoods and may contribute to growth via mechanisms like consumption smoothing, better creditworthiness, and investment in human capital and small enterprises." — Econstor, 2024

The key insight here is that the way recipients use remittances matters enormously. Families who channel even a portion into education or micro-enterprises create ripple effects that go far beyond their own household. If you want to understand how to support that process, exploring resources on turning remittances into savings projects can give you practical frameworks to share with your family.

Pro Tip: Encourage your family to set aside even 10% of each transfer into a dedicated savings account or cooperative fund. Over 12 months, that small habit can accumulate enough capital to fund a small business or pay for a year of higher education.

Now that we know remittances are not just short-term aid, let's see how these flows ripple through entire economies.

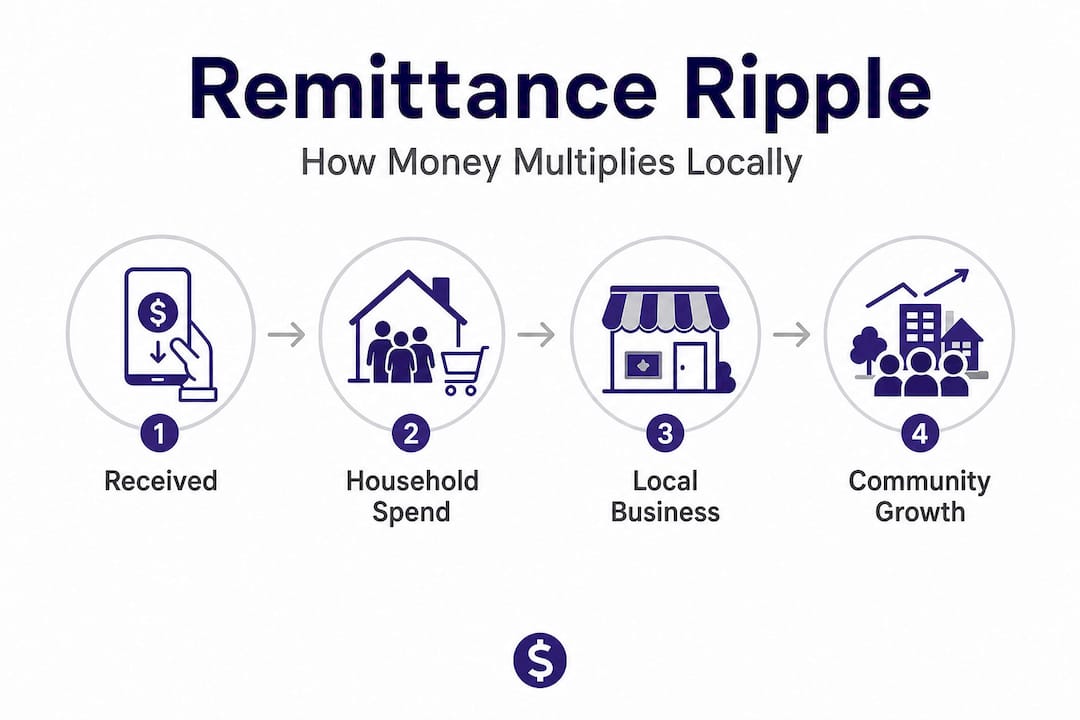

How remittance injects growth into the local economy

When thousands of households in a region all receive regular transfers, the combined effect on the local economy becomes significant. Think of it like a slow but steady pump filling a reservoir. Individual drops seem small, but the reservoir eventually overflows into surrounding farmland.

Research on remittance macroeconomic effects shows that average remittance inflows produce a positive macroeconomic effect for receiving countries, including a cumulative remittance-to-GDP multiplier and stronger investment over multiple years. In plain terms, every dollar sent home generates more than one dollar of economic activity locally because it gets spent, re-spent, and invested.

Remittance-to-GDP multiplier over 10 years (illustrative summary):

| Year | Estimated multiplier effect | Key driver |

|---|---|---|

| Year 1 | 1.1x to 1.3x | Direct household spending |

| Year 3 | 1.4x to 1.6x | Business investment and hiring |

| Year 5 | 1.7x to 2.0x | Education returns enter workforce |

| Year 10 | 2.0x to 2.5x | Compounded enterprise and human capital growth |

These numbers illustrate why economists take remittances seriously as a development tool, not just a social safety net.

How remittance prompts broader economic activity:

- Recipient households spend on local goods and services, boosting demand for local producers.

- Local businesses hire more workers to meet increased demand, reducing unemployment.

- New workers earn wages and spend locally, creating a second round of economic activity.

- Some households invest in small enterprises, adding productive capacity to the local economy.

- Education investments raise the skill level of the next generation, improving long-run productivity.

One striking data point: a one standard deviation income shock to migrant earnings can raise community investments in education and small enterprises, triggering longer-run virtuous growth cycles. That means when you get a raise or a bonus abroad and send more home, the effect on your home community is not linear. It compounds.

For diaspora communities interested in pooling resources for even greater impact, learning about entrepreneurial funding with remittances through cooperative models is worth exploring.

Economic growth is not the only story. For some communities, remittance inflows even reshape local markets and currency values, and that is where things get complicated.

Exchange rates, competitiveness, and the 'Dutch disease' debate

Here is something most remittance guides never explain: sending money home can actually make it harder for your home country to compete in global trade. This phenomenon has a name. Economists call it Dutch disease.

Dutch disease occurs when a large inflow of foreign currency, whether from oil revenues, aid, or remittances, causes the home country's currency to appreciate. A stronger currency sounds like good news. But it makes locally produced goods more expensive for foreign buyers, which can shrink export industries and cost jobs in manufacturing and agriculture.

Research confirms that remittances can appreciate the REER (real effective exchange rate), with potential Dutch disease effects, but outcomes vary significantly by exchange rate regime and the structure of the local economy.

Effects under different exchange rate regimes:

| Exchange rate regime | Currency appreciation risk | Export competitiveness impact | Overall growth risk |

|---|---|---|---|

| Flexible (floating) | High | Moderate to significant | Moderate |

| Fixed (pegged) | Low to moderate | Lower | Low |

| Mixed or managed float | Variable | Context-dependent | Variable |

Countries with fixed or managed exchange rates, like Morocco's dirham peg, tend to absorb remittance inflows with less currency volatility. Countries with fully floating currencies can see more dramatic appreciation when remittance volumes spike.

Factors that determine whether competitiveness suffers or benefits:

- The size of remittance inflows relative to the total economy (GDP share)

- Whether the country has a diversified export base or relies on one or two sectors

- How well local financial institutions channel funds into productive investment

- Government policies on foreign exchange and capital controls

- The degree to which remittances fund tradable goods production versus pure consumption

"Remittances can appreciate the real exchange rate, with potential Dutch disease effects, but outcomes vary by exchange regime and economy structure." — IMF Working Paper, 2025

The bottom line is that the relationship between remittance and exchange rates is not simple. The same flow of money that lifts one community can create structural challenges for another. Context is everything.

Why household choices and financial access matter

So why do some places see booming local businesses while others face economic risks from the same remittance flows? The answer often lies in what happens after the money arrives.

Channeling funds into investment can offset Dutch disease risks and promote tradable-sector expansion. In other words, the difference between a remittance that helps and one that creates problems often comes down to whether recipients invest or simply consume.

How households typically decide between consumption, saving, and investment:

- Immediate financial pressure (debt, medical bills) pushes toward consumption

- Access to savings products encourages setting money aside

- Availability of credit and business support services enables investment

- Financial literacy and awareness of options shapes long-term behavior

- Community norms around cooperative saving (like tontines) can redirect funds productively

Financial access is a major factor. In communities where banks are distant, fees are high, or accounts require minimum balances that most families cannot meet, remittances tend to flow straight into consumption. That is not a moral failing. It is a structural constraint. When families have access to savings groups, mobile banking, or cooperative credit, they are far more likely to put a portion of transfers to productive use.

"Remittance's local-economy impact is conditional on household behavior and constraints; channeling funds into investment can offset Dutch disease risks and promote tradable-sector expansion." — Journal of Economics, 2025

The role of diaspora financial solidarity is also worth noting. Collective savings models, where groups of migrants pool contributions and rotate lump-sum payouts to members, have been used for generations across African and Asian diaspora communities. These models provide capital access that banks often do not. If you want to explore how these systems work and how to connect your family to them, resources on diaspora financial solidarity offer practical starting points.

Pro Tip: When choosing a remittance service, look beyond the transfer fee. Some platforms partner with savings products or microfinance institutions in recipient countries. Sending through these channels can help your family access financial tools, not just cash.

What most remittance guides miss—and what senders should actually do

After reviewing the research and talking with thousands of senders, one pattern stands out clearly: most guides treat remittance as a purely financial transaction. Send money. Done. But the economic evidence tells a very different story.

The biggest missed opportunity is not the transfer fee. It is the lack of guidance that travels alongside the money. When you send $300 home, you have a choice. You can send just the money, or you can send the money plus a conversation about how to use it. That second option is almost always more valuable over time, yet almost no one does it intentionally.

Here is the uncomfortable truth: overuse of remittances for short-term consumption, while understandable, is one of the main reasons some communities do not see the long-term economic gains that the research says are possible. Families stuck in a cycle of using transfers only for bills and groceries never build the savings buffer or business assets that would make them less dependent on transfers in the first place.

The practical wisdom here is not to judge recipients. It is to recognize that you as the sender have more influence than you think. Encouraging your family to join a local savings cooperative, explore mobile savings accounts, or even set aside a small emergency fund can shift the trajectory of how your money works over years.

Another real pitfall is ignoring local banking and cooperative options entirely. Many senders focus only on finding the cheapest transfer service, which is absolutely important, but stop there. The last mile, meaning what happens to the money once it arrives, is just as important as the transfer cost.

Exploring tools like diaspora finance automation shows how technology is now helping diaspora communities manage collective savings more efficiently, reducing the administrative burden that used to make these models hard to sustain.

Pro Tip: Whenever possible, send information or tools alongside dollars. Share links to financial education resources, help your family understand how to open a savings account, or introduce them to a local cooperative. Money multiplies when it has a plan.

Send smarter: The next step for your family and community

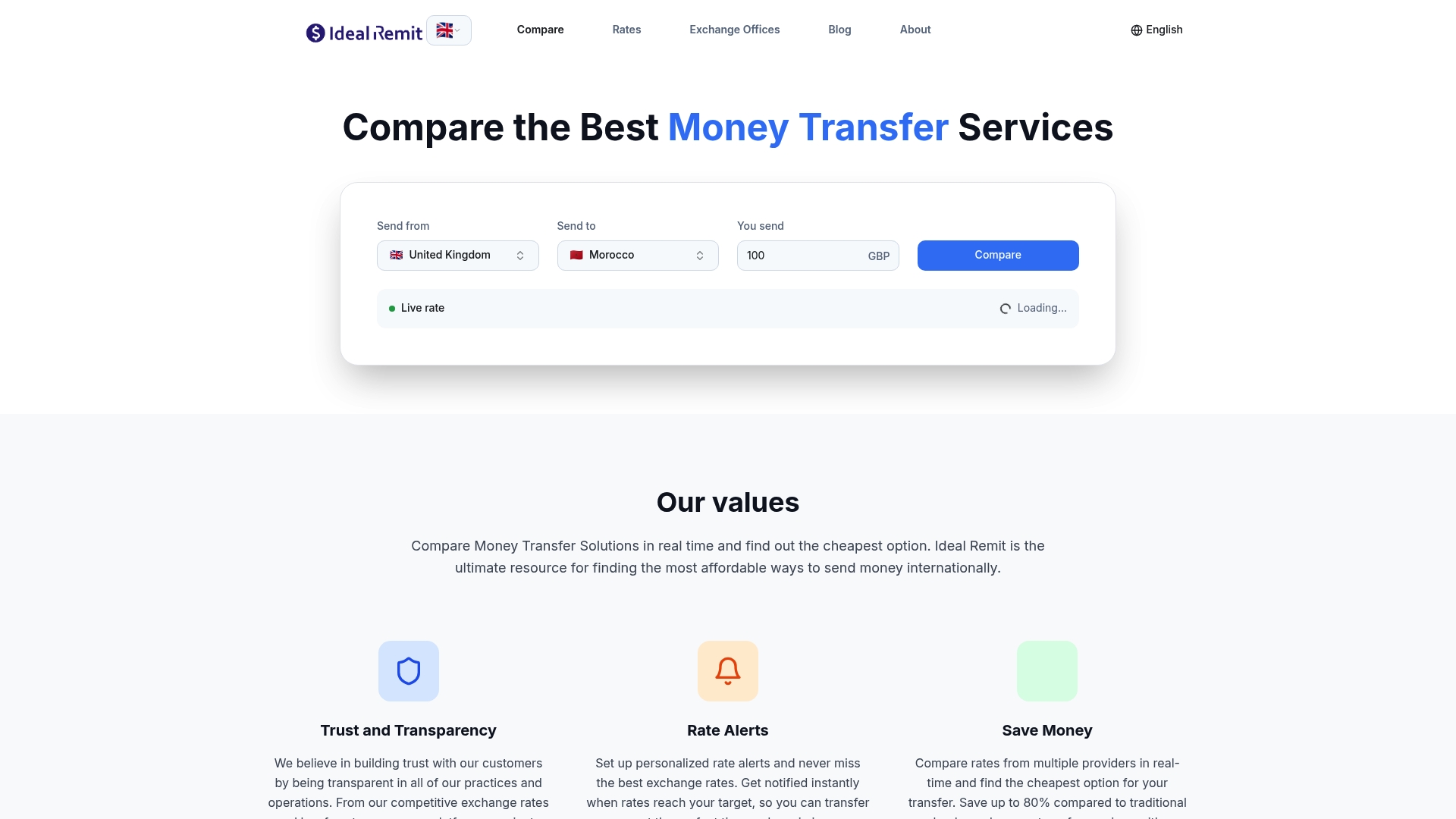

Understanding the economic impact of remittances is only valuable if it changes how you act. The first practical step is making sure you are not losing money unnecessarily on fees and poor exchange rates before your transfer even reaches your family.

At Ideal Remit, you can compare real-time rates and fees from leading transfer services side by side, including Western Union, MoneyGram, Remitly, Wise, and many others. The platform shows you exactly how much your family will receive after all costs, so you can choose the option that puts the most money in their hands. With potential savings of up to 80% compared to traditional bank transfers, and coverage across more than 100 countries, Ideal Remit gives you the transparency and tools to send smarter. Set up rate alerts, track live exchange rates, and make every transfer count for your family and your community.

Frequently asked questions

How do remittances affect economic growth?

Remittances boost economic growth by increasing local spending and investment, creating a multiplier effect over time. Remittance inflows produce a cumulative macroeconomic multiplier on GDP and investments that strengthens over multiple years.

Can remittances make recipient countries less competitive internationally?

Yes, large remittances can strengthen the local currency, which sometimes hurts export competitiveness under certain conditions. Remittance flows can appreciate the real exchange rate, with possible Dutch disease effects depending on the exchange rate regime.

What determines if remittance money is used productively?

Outcomes depend on household choices, local financial systems, and policies that help turn funds into investments or business development. Remittance's macro impact is conditional on household behavior and financial access, meaning structural support matters as much as the amount sent.

Do remittance effects last for years or are they only short-term?

Remittance shocks have effects that can last years, creating ongoing benefits for local economies well beyond the initial transfer. Dynamic persistence means remittance effects endure across multiple years, especially when funds are channeled into education and enterprise investment.

Written by

Brahim Oubrik

Brahim Oubrik, a senior data engineer who experienced firsthand the challenges of sending money internationally. Living in France while supporting his family in Morocco, Brahim regularly needed to transfer funds across borders. Drawing on his background in data engineering, Brahim decided to solve this problem not just for himself, but for the millions of others navigating the same difficulties. He built Ideal Remit to bring clarity to the international money transfer market.