TL;DR:

- Sending money internationally can unexpectedly cost 5% to 8% due to hidden fees and exchange rate markups. Comparing total costs, including fees and currency margins, and choosing bank transfers over cards can significantly reduce expenses. Using real-time comparison tools helps identify the cheapest providers tailored to your corridor and sending habits.

Sending money internationally sounds simple until you see what actually arrives on the other end. Hidden exchange rate markups, variable transfer fees, and confusing delivery options can quietly drain 5% to 8% of every transfer if you pick the wrong provider. This guide gives you a practical list of low-cost transfer providers, ranked by what actually matters: total cost, transparency, and real-world usability for expats, immigrants, and anyone sending regular remittances. You'll learn exactly what to compare, who the top players are, and how to pick the right one for your specific corridor and sending habits.

Table of Contents

- Key takeaways

- What to look for in a list of low-cost transfer providers

- Detailed profiles of the top providers

- Side-by-side comparison of costs and methods

- Choosing the right provider for your situation

- My honest take on navigating the low-cost transfer market

- Find your best rate with Idealremit

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Total cost is what matters | Compare transfer fees plus exchange rate markups together, not just the upfront fee. |

| Funding method changes pricing | Bank or ACH transfers are typically cheaper than card payments across most providers. |

| Corridor affects your best option | The cheapest provider for USD to EUR may not be cheapest for USD to MXN or USD to PHP. |

| "No fee" is not always free | Some providers skip the transfer fee but apply a markup on the exchange rate instead. |

| Comparison tools save real money | Using a dedicated comparison platform can cut transfer costs by up to 80% versus banks. |

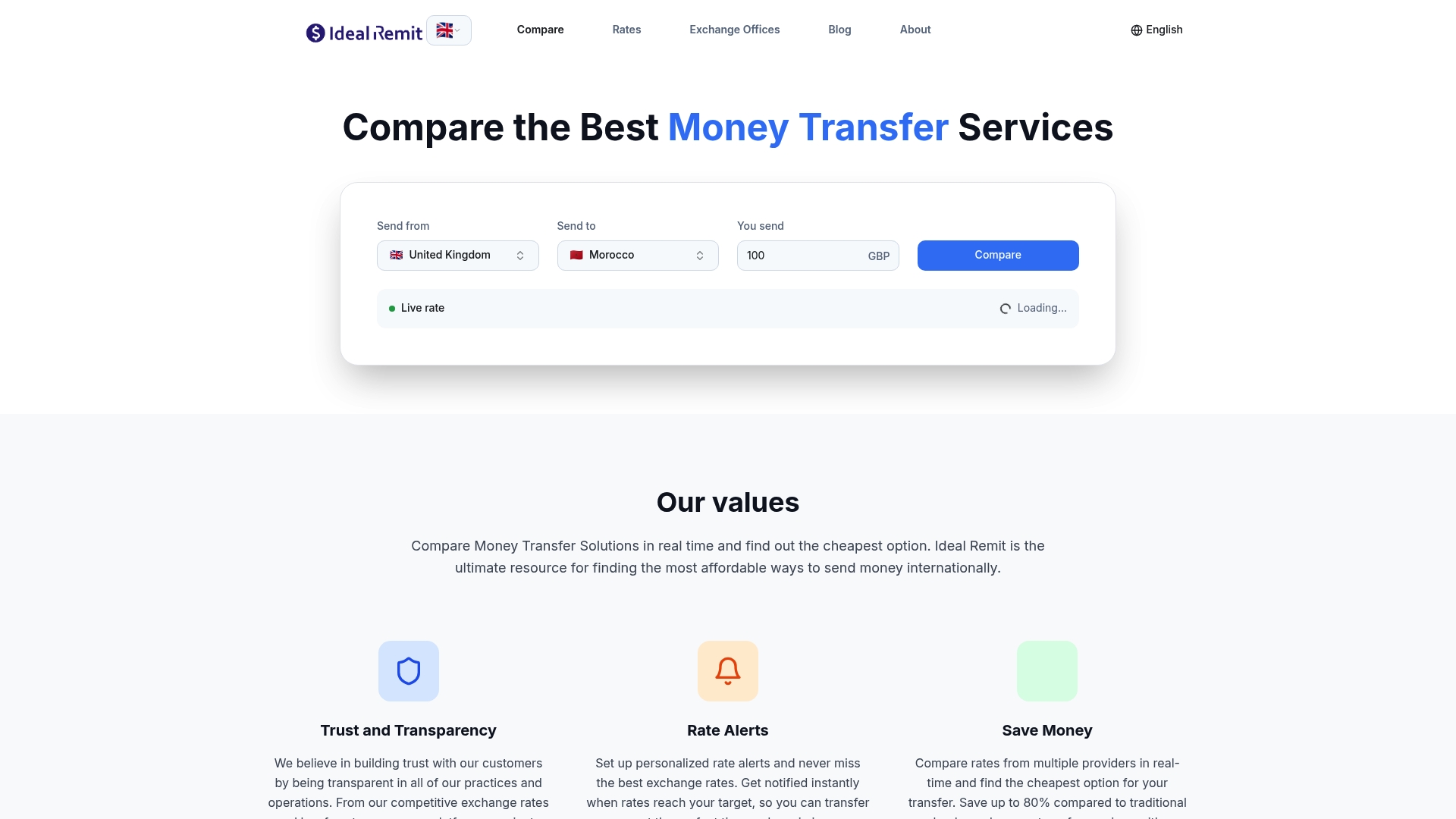

What to look for in a list of low-cost transfer providers

Not every provider is equally affordable for every situation. Before you bookmark any list of affordable money transfer services, you need to understand the factors that actually drive cost.

Total cost is fees plus exchange rate markup. A provider advertising "zero fees" may still profit by offering you an exchange rate worse than the mid-market rate. Avoiding exchange rate markups combined with transparent fee display is the primary driver of lower total costs. Always calculate what the recipient receives, not just what you pay.

Your funding method shifts the price. Paying by debit card or credit card almost always costs more than funding via bank transfer or ACH. Bank ACH funding is both cheaper and more predictable, making it the smarter choice for expats and immigrants sending recurring remittances.

Delivery method also affects fees. Bank deposits typically cost less than cash pickup. Mobile wallet delivery sits somewhere in between, depending on the corridor.

A few other criteria worth checking:

- Transfer speed: Same-day delivery usually costs a premium. Know whether you need speed or savings.

- Transfer limits: Some providers cap daily or monthly volumes, which matters for large sums.

- Fee transparency: Does the provider show you the full cost before you commit? If not, that's a red flag.

- Security and reliability: Look for providers regulated by FinCEN, FCA, or equivalent authorities.

Pro Tip: Before sending, always use the provider's live cost calculator for your exact corridor and funding method. Generic reviews often quote best-case scenarios, not what you'll actually pay.

Detailed profiles of the top providers

Wise

Wise uses the mid-market exchange rate with no markup, then charges a small transparent percentage fee on top. For a $1,000 transfer to Pakistan, fees start as low as $7.06 using bank or Wise account funding, making it one of the most cost-efficient options for that corridor. Wise also runs zero-fee promotions on transfers up to $2,000 to select currencies including EUR, INR, and PHP, though these offers change by route and timing.

Personal accounts can send up to $50,000 in 24 hours via ACH, with a 60-day rolling cap of $250,000. The rate is guaranteed at the moment you authorize the transfer, which protects you from rate swings during processing.

OFX

OFX charges no transfer fee at all, which sounds like a win. The catch is that it makes money through an exchange rate margin. For large transfers above $5,000, though, the spread is often narrow enough to make OFX genuinely competitive. It works best for business senders or individuals moving significant sums to countries like Australia, the UK, and Canada.

Xoom (a PayPal service)

Xoom is fast, often delivering within minutes to major corridors in Latin America and Asia. Upfront fees are low or sometimes waived, but the exchange rate markups are where Xoom adds cost. For small, urgent transfers where speed matters more than squeezing out every cent, it performs well. For large or frequent sends, the markup adds up.

MoneyGram and Western Union

These two networks cover more countries and cash pickup locations than almost anyone else. That reach comes at a price. Transfer fees vary significantly depending on your payment method and delivery choice, and exchange rate margins can be substantial. The sweet spot for both networks is when your recipient needs cash in hand in a country where digital delivery isn't reliable. If a bank account is available, there are almost always cheaper options.

Pro Tip: With Western Union and MoneyGram, always compare the online cost against the in-person agent cost. The same transfer can differ by several dollars depending on how and where you initiate it.

Revolut

Revolut offers low exchange rate markups and free transfers between Revolut users. On its free plan, weekend transfers and amounts above a monthly limit trigger a small markup. Upgrading to a paid plan unlocks better rates and higher limits. For expats already using Revolut for everyday spending, it doubles well as a cheap remittance option.

Zobo Money

Zobo targets the African diaspora specifically. It charges zero transaction fees and shows the full cost upfront, but the real cost depends heavily on the specific corridor. Ghana, Nigeria, Kenya, and Senegal are well-supported. If you're sending to sub-Saharan Africa and most providers feel expensive or unreliable, Zobo is worth checking directly for your route.

Side-by-side comparison of costs and methods

The table below gives you a practical framework for comparing providers on a $1,000 transfer across common corridors. Exact rates shift daily, so treat these as directional benchmarks and verify current figures before sending.

| Provider | Typical transfer fee | Exchange rate markup | Best funding method | Best for |

|---|---|---|---|---|

| Wise | $3 to $12 | 0% (mid-market) | ACH / bank transfer | Transparency, most corridors |

| OFX | $0 | 0.5% to 1.5% | Bank transfer | Large transfers |

| Xoom | $0 to $4.99 | 1% to 3% | Debit/credit card | Speed to LatAm, Asia |

| Western Union | $0 to $10+ | 1% to 4% | Bank transfer | Cash pickup, wide reach |

| MoneyGram | $0 to $10+ | 1% to 4% | Bank transfer | Cash pickup globally |

| Revolut | $0 (within limits) | 0% to 0.5% | Revolut balance | Expats with Revolut accounts |

| Zobo Money | $0 | Corridor-dependent | Bank transfer | Africa-focused corridors |

The cheapest transfer option flips depending on your corridor and delivery method. USD to INR via bank deposit plays out very differently in total cost versus USD to NGN via cash pickup, even with the same provider.

Pro Tip: Always run both the bank-funded and card-funded quotes side by side before finalizing. On a $1,000 transfer, the funding method alone can change your total cost by $10 to $30 with some providers.

Choosing the right provider for your situation

No single provider wins for everyone. The right pick depends on how often you send, how much, and where.

For frequent senders: Predictability matters as much as price. Providers that guarantee the exchange rate at authorization remove the uncertainty of rate swings during processing. Wise and OFX both work well here, with OFX offering relationship managers for regular high-volume senders.

For large sums: When moving $5,000 or more, even a 0.5% difference in exchange rate markup adds $25. OFX and Wise are typically the strongest contenders. Avoid funding large transfers by credit card regardless of the provider, as cash advance fees from your card issuer can stack on top of the transfer cost.

For small or occasional transfers: Xoom or Revolut often win on convenience and speed, especially to Latin America, India, or the Philippines. The exchange rate margin is less painful on a $200 transfer than on a $2,000 one.

For cash-dependent recipients: Western Union and MoneyGram remain unmatched for sheer physical reach. If your family picks up cash at a local agent in a rural area, these networks are often the only practical option.

- Expats sending to Europe: Wise and Revolut lead on cost and convenience.

- Immigrants sending to Africa: Zobo Money and Wise are strong depending on the country.

- Immigrants sending to Asia: Wise, Xoom, and Revolut are all worth comparing corridor by corridor.

- Casual senders who send once or twice a year: Use a comparison tool first, then pick. The best option shifts with exchange rate movements.

Using a comparison of transfer providers that shows real-time fees and exchange rates cuts through the noise fast, especially when the optimal choice changes with market conditions.

My honest take on navigating the low-cost transfer market

I've spent years watching people pay more than they should simply because a provider's marketing led with "no fees." The real cost was sitting in the exchange rate the whole time. When I look at what actually saves people money, the pattern is consistent. Providers that show you the mid-market rate and charge a transparent fee on top are almost always cheaper in total than those hiding their margin in the conversion.

The other thing I've seen trip people up is treating cheap remittance options as fixed. The best provider for your corridor six months ago may not be the best one today. Exchange rate volatility, promotional offers, and pricing changes shift the rankings regularly. I always recommend running a fresh comparison before any significant transfer.

My advice: fund with ACH or bank transfer whenever possible, avoid cards unless speed is the priority, and never take a "no fee" headline at face value without checking the rate you're actually getting. Staying informed and using a real-time comparison tool is the most reliable way to consistently get the best deal.

— Brahim

Find your best rate with Idealremit

Idealremit was built specifically for this problem. Instead of visiting six provider websites and trying to mentally compare exchange rates and fees across different corridors, you get everything in one place. The platform pulls live rates and fees from a wide network of trusted providers including Wise, MoneyGram, Western Union, Remitly, and others, and shows you the real total cost per transfer. You can filter by corridor, delivery method, and speed. You can also set rate alerts so you send when the conditions favor you most. For anyone serious about finding the cheapest transfer for their specific route, it's the fastest way to stop overpaying.

Start comparing at Idealremit and see exactly how much you could save on your next transfer.

FAQ

What is the cheapest way to send money internationally?

The cheapest method depends on your corridor and funding source. Using ACH or bank transfer with a provider like Wise typically delivers the lowest total cost due to mid-market exchange rates and transparent fees.

Why do "no fee" transfers still cost money?

Providers that advertise zero fees usually recover their margin through exchange rate markups. The recipient gets fewer local currency units than the mid-market rate would deliver, which is the hidden cost most senders miss.

How do I compare transfer providers accurately?

Always compare the total amount the recipient receives, not just the listed fee. Use a real-time comparison tool like Idealremit to see live rates and fees side by side across multiple providers for your exact corridor.

Does the funding method really affect transfer cost?

Yes, significantly. Card-funded transfers can cost $10 to $30 more on a $1,000 send compared to ACH or bank funding. Some providers also apply a separate card processing fee on top of the standard transfer fee.

How often should I re-check the best low-cost transfer provider?

Check before every significant transfer. Exchange rates, promotional offers, and provider pricing change regularly, so the best low-cost transfer services for your corridor today may not be the same next month.