Mobile money for global transfers: save more, send smarter

TL;DR:

- Mobile money offers significantly lower international transfer fees compared to traditional banks and can provide instant, flexible transfer options without needing a bank account.

- Despite its cost-effectiveness, awareness, habits, and regulatory barriers prevent most users from adopting mobile money for cross-border remittances.

- Careful comparison of funding and payout methods along with understanding corridor-specific costs can maximize savings and efficiency in international mobile money transfers.

Mobile money transfers cost nearly half what traditional banks charge for sending money internationally, yet most individuals and small businesses still default to their bank out of habit. The gap is striking: while banks average over 8% in fees for cross-border transfers, mobile money solutions can bring that figure down dramatically. This guide breaks down exactly how mobile money works, what the real cost comparisons look like, how to execute an international transfer step by step, and the less obvious factors that most senders completely overlook when choosing their transfer method.

Table of Contents

- What is mobile money and how does it work?

- Comparing costs: Mobile money vs traditional transfer methods

- How mobile money enables international transfers

- Wider impact: Financial inclusion and economic growth

- Why cost isn't the only factor: Nuances most senders miss

- Explore cost-effective mobile money transfers with IdealRemit

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cheapest transfer method | Mobile money often offers lower fees than traditional banks for sending money abroad. |

| Wider access | Mobile money enables transfers without needing a bank account, increasing financial inclusion. |

| Flexible payout options | You can receive international remittances in bank accounts, cash, or directly into a mobile wallet. |

| Regulatory challenges | Scaling international mobile money transfers may be limited by cross-border data and policy frictions. |

| Optimize by instrument | Cost savings depend on both how you fund the transfer and how the receiver accesses the funds. |

What is mobile money and how does it work?

Mobile money is a phone-based financial service that lets you store, send, and receive funds without needing a traditional bank account. Think of it as a digital wallet tied to your mobile number rather than a bank branch. You load money into your wallet either through a registered agent location (like a corner store or pharmacy) or by linking an existing bank account. From there, you can pay bills, buy goods, or send money to someone across town or across the world.

The agent network is the backbone of mobile money in many countries. Millions of small shop owners and kiosks serve as cash-in and cash-out points, meaning someone without a bank account can still participate fully in the digital economy. This is especially important in sub-Saharan Africa, South Asia, and parts of Latin America where digital financial inclusion remains a work in progress.

According to World.org, mobile money enables users to transfer, store, and request money from a phone, with agent locations handling cash deposits and withdrawals, supporting spending and transfers entirely outside the traditional banking system. That last part matters. You don't need a credit score or minimum balance. You just need a registered SIM card and an agent nearby.

For international transfers specifically, mobile money networks connect to global remittance rails. A sender in the UK can fund a transfer through their wallet or a debit card, and a recipient in Kenya or Senegal can receive it directly to their mobile wallet, at a bank branch, or as cash from an agent.

Here is a quick summary of the key features most mobile money platforms offer:

- Send and receive funds instantly to other wallet users

- Cash in and cash out at hundreds of thousands of agent locations globally

- Pay bills and merchants without carrying physical cash

- Receive international remittances from abroad into the wallet

- Link to bank accounts for added flexibility

- Set up savings groups or recurring transfers

For a deeper look at keeping your transfers safe, the secure money transfer guide at IdealRemit covers the most important security practices.

Key insight: Mobile money removes the need for a formal banking relationship, which is why it has become the primary financial tool for over a billion people globally.

Comparing costs: Mobile money vs traditional transfer methods

Now that the mechanism is clear, let's talk about what you actually pay. The fee difference between mobile money and traditional bank transfers is not marginal. It is substantial enough to significantly affect how much money actually reaches your recipient.

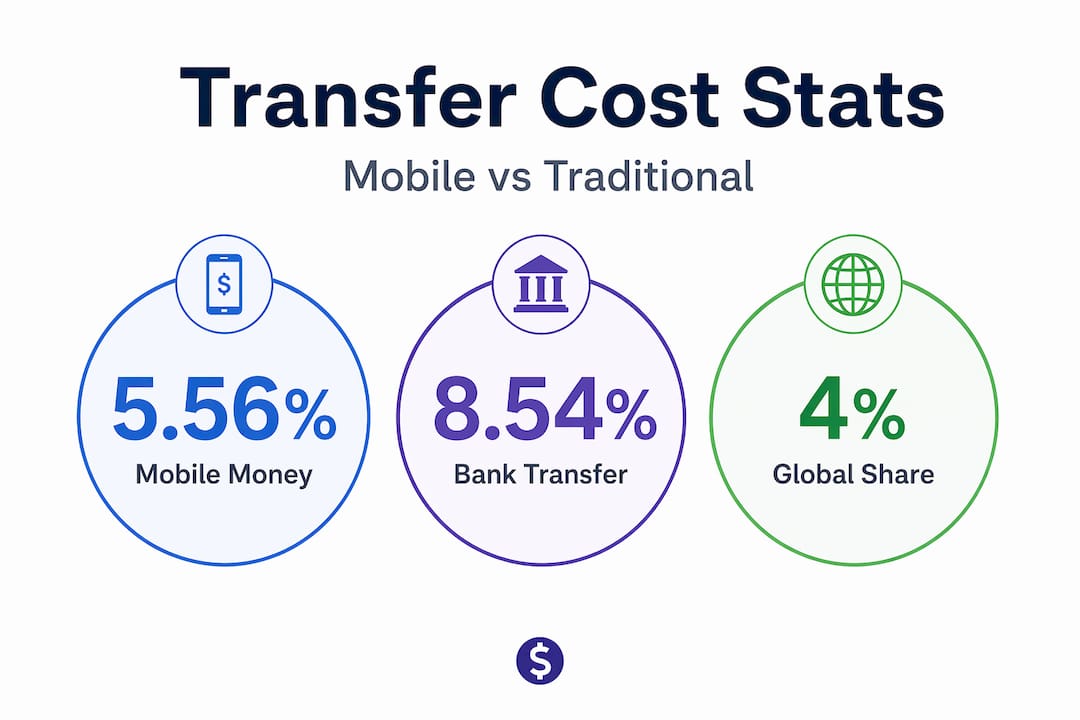

According to Q3 2024 World Bank data, sending via mobile money averaged 5.56%, compared to 8.54% when sending via bank account. Receiving to a mobile wallet averaged just 4.46% across 470 services tracked in the same period. On a $500 transfer, that difference between 5.56% and 8.54% is about $15 in real money. Over a year of regular remittances, those savings add up fast.

Here is how the major transfer methods compare across key cost dimensions:

| Transfer method | Average sending fee (Q3 2024) | Speed | Bank account required? |

|---|---|---|---|

| Mobile money (sending) | 5.56% | Minutes to hours | No |

| Bank account (sending) | 8.54% | 1 to 5 business days | Yes |

| Receiving to mobile wallet | 4.46% | Minutes | No |

| Receiving to bank account | Varies (often higher) | 1 to 3 business days | Yes |

| Cash pickup | Varies by corridor | Minutes | No |

One important data point: despite being cheaper, mobile money accounts for just 4% of global remittance flows. This gap between cost efficiency and actual usage tells you something important. Awareness, habit, and regulatory barriers are keeping the majority of senders on more expensive rails.

The cross-border transfer cost average for mobile money remittances in 2024 sat at 3.54%, well below the G20's 5% target for global remittance costs. Banks still have not hit that target on average.

Pro Tip: Do not just compare "mobile money vs bank." Compare by direction too. Receiving to a mobile wallet (4.46%) is often cheaper than receiving to a bank account. Choosing the right receiving method can reduce costs as much as choosing the right sending method.

A few other factors drive cost differences beyond the base fee:

- Exchange rate markups added on top of the transfer fee

- Corridor-specific pricing (some routes are cheaper than others regardless of method)

- Flat fees vs. percentage fees (flat fees favor larger transfers; percentage fees favor smaller ones)

- Promotional rates offered by digital-first providers competing for market share

For ongoing money transfer insights and live rate comparisons, IdealRemit tracks these variables across dozens of providers so you can see the full picture before you commit. When you're ready to act, you can also compare transfer costs across real providers in seconds.

How mobile money enables international transfers

The actual process of sending money internationally via mobile money is more straightforward than most people expect. Here is how a typical transfer unfolds from start to finish:

- Register and activate your mobile wallet. Most services require a government ID and a phone number. Verification is usually completed within minutes.

- Load funds into your wallet. Use an agent location for cash, or link a debit card or bank account for direct top-ups.

- Select the international transfer option. Look for "Send Abroad," "Global Transfer," or similar in your wallet app.

- Enter the recipient's details. This includes their phone number, bank account, or agent location depending on the payout method they prefer.

- Review fees and exchange rate. A transparent service will show you the exact fee and the exchange rate before you authorize anything.

- Authorize via PIN or biometrics. Confirm the transfer with your security method, and the transaction is initiated immediately.

- Recipient receives funds. Depending on the corridor and payout channel, this can happen within seconds or take a few hours.

The M-Pesa Global guide illustrates this process clearly. Senders opt into the international feature, select their destination country, review the fee and exchange rate displayed before authorization, and confirm with a PIN or biometric. M-Pesa routes global transfers through Western Union's network, giving access to millions of bank accounts and payout locations worldwide.

Here is a comparison of the payout options your recipient typically has available:

| Payout method | Speed | Fee level | Bank account needed? | Best for |

|---|---|---|---|---|

| Mobile wallet | Instant to 2 hours | Lowest | No | Regular recipients with a wallet |

| Cash pickup | Minutes | Medium | No | Recipients without digital accounts |

| Bank account | 1 to 3 days | Medium to high | Yes | Larger amounts, formal transactions |

| Home delivery | Hours to 1 day | Higher | No | Elderly or mobility-limited recipients |

Worth noting: The payout method your recipient chooses can change the total cost of the transfer just as much as the method you use to send. This is one of the most overlooked levers for saving money on international transfers.

The ability to mix and match funding and receiving channels makes mobile money remarkably flexible. You can fund a transfer via mobile wallet and have it paid out as cash at an agent, or fund via bank card and deliver it directly to a mobile wallet. Visit transfer solutions blog for practical guides on optimizing each leg of the transfer.

Wider impact: Financial inclusion and economic growth

Beyond individual savings, mobile money is reshaping how entire economies function. For many households in developing countries, a mobile wallet is not just a transfer tool. It is their primary interface with the formal financial system.

Small businesses benefit particularly. A market trader in Accra can receive payments from suppliers in Lagos, pay staff wages digitally, and build a transaction history that can eventually qualify them for small business credit. None of that was possible with cash alone. The financial inclusion partner research highlights how community-based financial practices are increasingly integrating with mobile money platforms to extend access further.

The GSMA identifies several key growth drivers in this space. Higher transaction values and ecosystem use, including international remittances, are expanding the footprint of mobile money well beyond simple person-to-person transfers. Bill payments, merchant transactions, agricultural input payments, and government disbursements are all flowing through mobile money rails in mature markets.

The same GSMA research highlights interoperability as a critical issue. When mobile money systems from different providers and different countries can connect seamlessly, costs drop and access improves. Right now, many networks remain siloed, meaning a sender and recipient must often use the same provider to transact directly. Cross-border harmonization, the process of aligning regulatory and technical standards across countries, is what unlocks the next level of mobile money's potential.

Key factors shaping the future of mobile money for international transfers:

- Interoperability agreements between national mobile money systems

- Regulatory harmonization across sending and receiving countries

- Growing smartphone penetration enabling richer app experiences

- Diaspora communities driving demand for corridor-specific products

- Integration with savings groups and community finance tools as shown by digital diaspora solutions

However, regulatory friction is real. Cross-border data transfer rules in some jurisdictions make it harder for providers to operate across borders efficiently. This limits scale, which in turn keeps fees higher than they could be for certain corridors. The gap between what mobile money can do and what it currently does in international remittances is largely a policy gap, not a technology gap. Find more on inclusive transfer trends as this landscape continues to evolve.

Why cost isn't the only factor: Nuances most senders miss

Here is the perspective most articles skip. Focusing purely on the headline percentage fee is a shortcut that can lead you to the wrong choice.

The World Bank's Remittance Prices Worldwide report benchmarks costs by instrument and direction, not just by provider. This means the same provider can look expensive or cheap depending on where mobile money appears in the transaction chain. Are you sending via mobile money, or receiving via mobile wallet? Both matter separately. A corridor where sending via mobile money is costly might still be very efficient when receiving to a mobile wallet, and vice versa.

We have seen users assume that because "mobile money is cheaper," any transaction involving a mobile wallet will beat a bank transfer. That is not always true. The savings depend heavily on the specific sending country, the receiving country, and the funding and payout methods chosen. The combination matters more than any single variable.

Then there is the regulatory dimension. GSMA's research confirms that interoperability and cross-border harmonization remain unresolved, and that data transfer regulations actively constrain some providers from scaling their international mobile money services. This means in some corridors, even the most cost-efficient mobile money option simply isn't available or is limited in transfer amounts. Choosing a provider that operates confidently within your specific corridor matters far more than picking the one with the lowest headline fee.

Pro Tip: Always check both the funding channel and the receiving channel independently when comparing costs. Switching just the receiving method from bank to mobile wallet can sometimes save more than switching providers entirely.

The most financially savvy senders treat every transfer as a combination of variables: the amount, the corridor, the funding method, and the payout method. The expert transfer tips section at IdealRemit addresses each of these levers with current, corridor-specific guidance.

Explore cost-effective mobile money transfers with IdealRemit

Ready to apply these lessons and find your best transfer option?

IdealRemit makes it simple to compare mobile money options alongside all major transfer methods in real time. Whether you're sending $200 or $2,000, the platform aggregates live rates, fees, and exchange rate markups across trusted providers so you can see exactly what your recipient will receive.

For UK-based senders, compare best transfer rates to find the most affordable route for your specific corridor. US senders can compare US transfer services across dozens of providers instantly. For a global view of the cheapest global transfers available right now, the IdealRemit homepage gives you a starting point tailored to where you are and where you're sending. Savings of up to 80% compared to bank rates are available on many corridors. The numbers are there. You just need the right tool to find them.

Frequently asked questions

How does mobile money work for sending international transfers?

Mobile money lets you transfer funds from your phone wallet, bridging to bank accounts or cash payout channels globally through partner networks, without needing a traditional bank account.

Is sending money with mobile money cheaper than using a bank?

Yes. According to Q3 2024 World Bank data, sending via mobile money averaged 5.56% versus 8.54% via bank account, making mobile money consistently cheaper on most corridors.

Can I receive international transfers directly on my mobile money wallet?

Yes, many services support direct wallet payouts from abroad. Receiving to a mobile wallet averaged just 4.46% across 470 tracked services in Q3 2024, often the lowest payout fee available.

Are there any limitations or risks with mobile money for international transfers?

Yes. Regulatory barriers and data transfer rules can restrict international mobile money services in certain regions, and limited interoperability between networks means some corridors have fewer low-cost options than others.

Recommended

Written by

Brahim Oubrik

Brahim Oubrik, a senior data engineer who experienced firsthand the challenges of sending money internationally. Living in France while supporting his family in Morocco, Brahim regularly needed to transfer funds across borders. Drawing on his background in data engineering, Brahim decided to solve this problem not just for himself, but for the millions of others navigating the same difficulties. He built Ideal Remit to bring clarity to the international money transfer market.