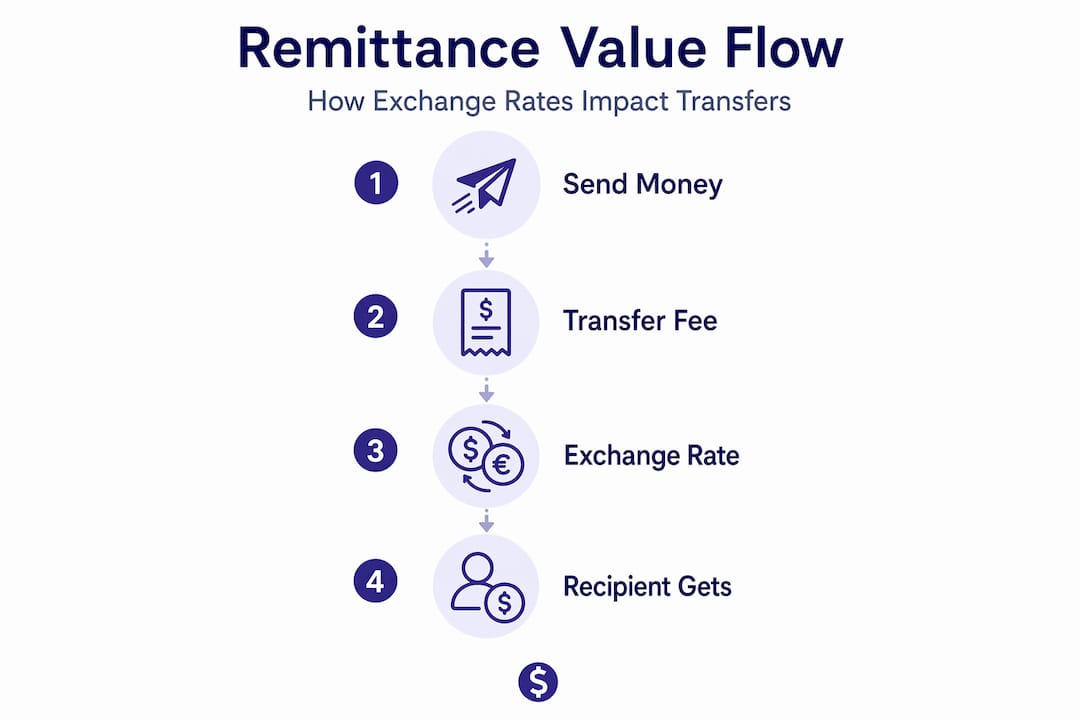

Why exchange rates matter for international remittances

TL;DR:

- The exchange rate used during remittance transfers has a greater impact on the recipient's value than the transfer fee itself. Small fluctuations in exchange rates can significantly reduce the actual amount received and affect the recipient’s purchasing power over time. Choosing providers that lock in rates and comparing final recipient amounts helps maximize remittance value amidst market volatility and inflation.

Most people sending money abroad spend a lot of energy hunting for the lowest transfer fee. That instinct is understandable, but it misses something bigger: the exchange rate applied to your transfer often has a far greater effect on what your family actually receives than the fee does. As exchange rate experts note, the FX rate largely determines how much foreign currency your recipient can buy, because those rates shift throughout the day. A fee of $5 is fixed. An exchange rate that moves just 1% on a $500 transfer wipes out $5 instantly, and that movement can happen in minutes.

Table of Contents

- How exchange rates affect your remittance's value

- What drives exchange rate fluctuations?

- Why exchange rates differ between money transfer providers

- Impact of timing and transaction delays on exchange rates

- Exchange rates and local inflation: What remittance senders should consider

- Why focusing only on fees misses the bigger remittance picture

- How IdealRemit helps you get the best exchange rates and maximize your remittances

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Exchange rates determine remittance value | The exchange rate used for currency conversion directly impacts how much your recipient receives in local currency. |

| Small shifts matter | Even minor exchange rate changes can significantly affect the purchasing power of money sent abroad. |

| Compare effective rates | Focus on total recipient payouts and effective exchange rates, not just transfer fees, to save more. |

| Timing affects outcomes | Exchange rate fluctuations and transfer delays expose remittances to value changes between sending and delivery. |

| Consider inflation impact | Local inflation influenced by exchange rates can erode the real value of remittances over time. |

How exchange rates affect your remittance's value

Why exchange rates matter becomes clearest when you look at specific numbers. Imagine you send $500 to a family member in Morocco. Provider A converts at 10.00 dirhams per dollar, so your family receives 5,000 dirhams. Provider B converts at 9.70 dirhams per dollar, so your family receives 4,850 dirhams. Both providers might advertise the same $4 fee, yet the rate difference costs your family 150 dirhams, roughly enough to cover a week of vegetables and bread.

That gap is not hypothetical. Small FX movements can noticeably change a family's purchasing power for essentials like groceries and medicine. When you are sending money every month, those differences stack up fast:

- Rate variability by hour: Exchange rates for popular corridors like USD to MAD or GBP to PHP can swing by 0.5% to 1% within a single business day.

- Cumulative effect for regular senders: A 0.5% rate disadvantage on $400 sent monthly equals roughly $24 lost per year. Across five years, that is $120, enough to fund school supplies for a child.

- Transfers processed at different times: A transfer queued at 9 a.m. may lock in a different rate than the same transfer submitted at 3 p.m., purely because markets moved.

- Local currency strength matters too: If the destination currency is weakening against the dollar, even a "good" rate today may deliver less real value than the same rate six months ago.

To properly assess total remittance cost, you need to look at both the fee and the rate together, not one without the other.

Pro Tip: Before you send, calculate the recipient amount in local currency rather than focusing on the dollar amount you are sending. That single habit reframes the entire comparison.

Understanding these shifts in value is the first step. With this impact in mind, let's explore what actually drives exchange rate changes and why they fluctuate so unpredictably.

What drives exchange rate fluctuations?

Exchange rates are not random. They respond to real economic forces, though those forces can move quickly and sometimes in surprising directions. Currency values shift based on interest-rate differentials, capital flows, trade balances, and market sentiment, which means watching a few key indicators gives you a meaningful edge.

Here are the five main forces behind the movements you see when you check rates before sending:

- Interest rate differences. When a country raises its benchmark interest rate, its currency typically attracts more foreign investment, pushing the currency's value up. The U.S. Federal Reserve's decisions, for example, ripple instantly into exchange rates for USD-to-peso or USD-to-dirham corridors.

- Trade balances. A country that exports more than it imports sees stronger demand for its currency. The opposite, a trade deficit, can weaken a currency over time. If the destination country runs a large deficit, its currency may slowly lose value against the dollar.

- Political and fiscal stability. Elections, policy changes, and government debt levels all influence investor confidence. A country that looks politically unstable sees capital leave quickly, weakening its currency sharply and often without warning.

- Market sentiment and risk appetite. During global uncertainty, investors flee to "safe haven" currencies like the U.S. dollar or Swiss franc. This can cause dramatic swings in emerging market currencies even when nothing has changed in that specific country.

- Central bank announcements. A single statement from a central bank about future policy can move a currency by 1% to 2% in hours. If you send money the day before a major announcement and the rate moves against you, your family receives less, even though you could not have predicted it.

Understanding these factors helps you manage currency fluctuations more deliberately, watching for major economic news before committing to a large transfer.

Why exchange rates differ between money transfer providers

Not all providers show you the same rate, even if you check them at the exact same moment. The explanation starts with something called the mid-market rate, which is the midpoint between what buyers and sellers pay for a currency. It is the "real" rate you see on Google or Reuters, and no retail sender gets it automatically.

Every provider takes that mid-market rate and adds a markup. That markup is where hidden FX costs live, and higher operating costs can lead to wider FX margins that quietly shrink your family's payout. A traditional bank with thousands of physical branches passes those overhead costs directly to you through a wider margin. A leaner digital provider may pass on a much tighter margin, even if its fee looks similar.

Here is a simplified comparison to illustrate how rates and fees interact on a $400 transfer to Morocco:

| Provider | Exchange rate (USD/MAD) | Transfer fee | Recipient receives |

|---|---|---|---|

| Traditional bank | 9.50 | $5.00 | 3,800 MAD |

| Provider A (digital) | 9.85 | $4.00 | 3,936 MAD |

| Provider B (digital) | 9.75 | $0.00 | 3,900 MAD |

| Provider C (digital) | 10.00 | $6.00 | 3,976 MAD |

The bank looks cheap on fees but delivers the least. Provider C charges the highest fee but delivers the most. This is why remittance pricing explained in full detail always comes back to one number: the final recipient amount, not the advertised fee.

Pro Tip: Always use a comparison tool that shows you the recipient amount in local currency after fees and exchange rate markup. That single figure tells you everything.

Knowing these cost components empowers you to compare providers effectively and maximize what your family receives. But there is one more layer: timing.

Impact of timing and transaction delays on exchange rates

Even after you pick the best provider and rate, the moment your money actually converts can differ from the moment you hit "send." This gap creates real risk.

Cross-border payment systems, especially those sending money into regions with tighter financial regulations, can hold transfers for hours. According to IMF research from 2026, transaction delays increase exposure to exchange rate changes, meaning final payouts vary based on market moves during that delay window.

What this looks like in practice:

- Processing windows of 4 to 8 hours are common on corridors with capital controls or manual compliance reviews.

- Rate locks vs. rate-at-settlement: Some providers lock in your rate at the time you send. Others convert at the rate available when they settle the transfer. The difference matters enormously during volatile periods.

- Weekend and holiday timing: Transfers initiated on Friday afternoon may not settle until Monday, exposing you to a full weekend of potential movement without any ability to intervene.

- Recipient-side delays: Even when your provider settles quickly, local correspondent banks in the destination country can add further processing time, extending your exposure.

Delays of even a few hours can shift the final payout by 0.5% or more during periods of high volatility, which on a $600 transfer equals $3 to $6 in purchasing power for your family.

Smart remittance timing means understanding whether your provider offers a rate lock, and preferring providers that do when you are sending larger amounts or transferring during uncertain market periods.

Exchange rates and local inflation: What remittance senders should consider

Here is the part of the conversation most articles skip entirely. Even if you send money at a great exchange rate today, inflation in the destination country can quietly erode what that money buys.

Exchange rate changes influence inflation by affecting import prices, which in turn affect the real value of remittances over time. When a country's currency weakens against the dollar, imports become more expensive, and those higher costs flow through to grocery store prices, utility bills, and rent.

Key points to factor into your long-term remittance planning:

- A weakening local currency cuts both ways. Your family receives more units of local currency per dollar, but each unit buys less than it did before.

- Import-dependent economies feel this faster. Countries that import most of their food, fuel, or medicine see inflation respond sharply to currency movements.

- Historical purchasing power matters. If you have been sending the same dollar amount for three years, your family may be receiving more local currency now but affording roughly the same amount of goods due to inflation.

- Adjust amounts periodically. Review local inflation data in the destination country every six months and consider whether your transfer amount still covers the same basket of essentials.

- Remittance and inflation impact on household welfare is a real and measurable phenomenon, particularly in countries like Morocco, the Philippines, and Nigeria where remittances make up a significant share of household income.

Exchange rate timing alone may not guarantee stable purchasing power. The full picture requires watching both the rate you send at and the inflation your family faces when they spend it.

Why focusing only on fees misses the bigger remittance picture

Here is an opinion that the remittance industry rarely states plainly: the obsession with fees is partly a marketing problem that providers created. Advertising a $0 fee is a powerful headline. Disclosing a 3% exchange rate markup buried in a terms page is not. The result is that millions of senders make decisions based on the visible number while missing the larger, invisible one.

The key risk is not only fees. It is the FX rate used during conversion and how it moves between the moment you get a quote and the moment your money actually settles. That gap is where real money disappears without anyone lying to you.

Experienced senders learn to think in two parts: the explicit fee, which you can see, and the FX margin, which you have to calculate. Add them together to get the true cost. Experts caution that comparing total recipient payout instead of just advertised fees is the only reliable way to avoid hidden FX costs. Our view at Ideal Remit is that a sender who consistently applies this two-part test will save more over a year than one who chases zero-fee promotions.

There is also a timing dimension that most guides underestimate. Exchange rate volatility between quote and delivery adds risk you genuinely cannot control, but you can reduce it by choosing providers that lock in rates and by comparing remittance providers side by side on final recipient amounts rather than headline fees. That one shift in how you shop changes everything.

How IdealRemit helps you get the best exchange rates and maximize your remittances

Understanding why exchange rates matter is the foundation. Applying that knowledge every time you send is where the real savings happen.

Ideal Remit is built specifically for this problem. The platform lets you compare money transfer providers on actual recipient amounts, pulling together real-time exchange rates, fees, and estimated delivery times across trusted providers like Western Union, MoneyGram, Remitly, Wise, and more, all in one place. You can also set up personalized rate alerts so you send when the market moves in your favor. For practical strategies on keeping costs down, the Ideal Remit blog covers topics from timing your transfers to avoiding hidden markups. And if you want a quick starting point, this guide on saving on international transfers breaks down exactly how families save up to 80% compared to sending through a bank.

Frequently asked questions

What exactly is an exchange rate in remittances?

It is the rate used to convert your currency into your recipient's currency, directly determining how much they receive. An FX rate is the value of one currency compared to another, and even a small difference in that rate affects your family's purchasing power.

Why do different transfer providers offer varying exchange rates?

Providers add their own markup to the mid-market rate to cover costs and generate profit. Every company adds a markup to the real exchange rate, which is why comparing final recipient amounts rather than fees is the only accurate way to evaluate cost.

Can timing my transfer affect how much my recipient gets?

Yes, because rates shift constantly and processing delays expose your transfer to those movements before settlement. Transaction delays increase exposure to exchange rate changes, meaning the final payout can vary based on market conditions during processing.

How do exchange rates relate to inflation for remittance recipients?

Exchange rates affect how much imported goods cost, which feeds into local inflation and reduces what your family can buy over time. Exchange rate changes influence inflation through import prices, quietly eroding the real value of remittances even when the nominal amount stays the same.

Recommended

Written by

Brahim Oubrik

Brahim Oubrik, a senior data engineer who experienced firsthand the challenges of sending money internationally. Living in France while supporting his family in Morocco, Brahim regularly needed to transfer funds across borders. Drawing on his background in data engineering, Brahim decided to solve this problem not just for himself, but for the millions of others navigating the same difficulties. He built Ideal Remit to bring clarity to the international money transfer market.