TL;DR:

- Trustworthy remittance providers are regulated and licensed, with ongoing compliance monitoring to protect your money. Regulatory oversight requires licensing, anti-money-laundering programs, sanctions screening, and periodic audits that ensure operational transparency. Verifying registration, understanding fee structures, and reviewing privacy policies are essential steps to make safe, informed money transfers.

When you send money home, it's easy to assume that choosing a familiar logo means your transfer is safe. That's the misconception the role of trusted providers in remittance quietly exposes. Real trust has nothing to do with brand recognition and everything to do with government licensing, anti-money-laundering compliance, and operational transparency. This guide breaks down what actually makes a remittance provider trustworthy, why those regulatory layers protect your money, and how you can verify you're using a provider that meets the standard your family depends on.

Table of Contents

- How regulation shapes trust in remittance providers

- Country-specific requirements that guarantee provider accountability

- Transparency and privacy: modern pillars of trust for remittance users

- Reliability and service features that trusted providers deliver

- Comparing trusted remittance providers: fees, privacy, and service quality

- Practical tips to ensure your remittance provider is truly trusted

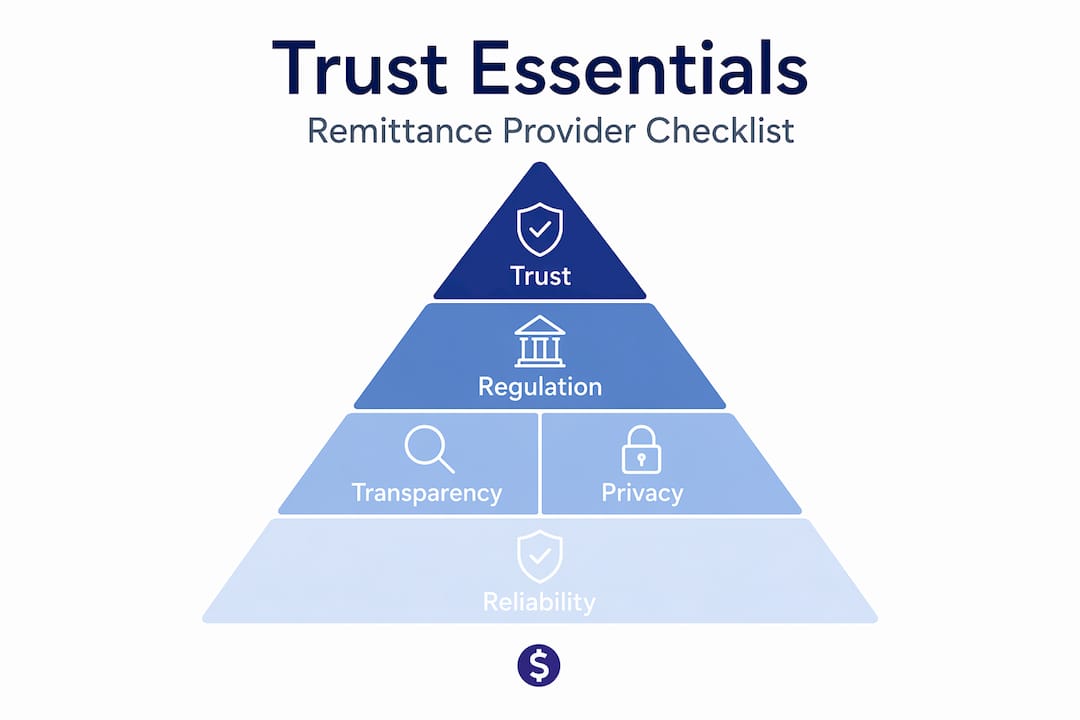

- Why trust in remittance providers goes beyond brand reputation

- Find the best trusted remittance provider for your transfers

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Regulatory compliance | True trust in remittance depends on providers being licensed and actively monitored by authorities. |

| Transparency matters | Clear fee disclosure and privacy safeguards are essential for trusting remittance apps. |

| Operational reliability | Providers offering tracking and fraud protection reduce risks of payout failures. |

| Check payout methods | Confirm recipient delivery options and timing before sending money. |

| Evidence-based trust | Trust is built on documented compliance and clear operational controls, not just brand familiarity. |

How regulation shapes trust in remittance providers

Most people think of "trust" in financial services as a gut feeling. In remittance, it's a legal requirement. Every provider handling cross-border money transfers operates within a global framework that mandates licensing, monitoring, and compliance, not as optional best practices but as conditions for operating legally.

The Financial Action Task Force (FATF), the global standard-setter for combating financial crime, makes this explicit. MVTS providers must be licensed and monitored under AML/CFT (anti-money laundering and counter-terrorist financing) regimes to prevent their networks from being used for illicit finance. That's not marketing language. That's a gatekeeping requirement with real teeth.

Here's what regulatory oversight actually involves for remittance providers:

- Licensing approval before they can legally accept your money

- Ongoing AML programs that require them to identify customers and flag suspicious activity

- CTF screening against government sanctions lists to block prohibited transactions

- Suspicious transaction reporting to national financial intelligence units

- Periodic compliance audits by supervisory agencies

- Oversight of agents and affiliates who process transfers on the provider's behalf

Operating without proper registration is illegal in most jurisdictions, and your money sent through an unregistered provider has virtually no protection if something goes wrong. The compliance structure isn't bureaucratic overhead. It's the mechanism that makes your transfer recoverable when problems arise.

Pro Tip: Before sending money, search your provider's name in your country's financial regulator database. In the U.S., that's FinCEN's MSB Registrant Search. In the UK, it's the FCA register. A provider not found there is a serious red flag. Review our international transfer security checklist for a full step-by-step verification process.

Country-specific requirements that guarantee provider accountability

Understanding these safeguards at the country level helps reveal why choosing registered providers matters for your transfers.

The rules aren't uniform globally, but two strong examples, Australia and the United States, show how serious governments are about holding remittance providers accountable through detailed, ongoing obligations.

How Australia structures remittance oversight:

AUSTRAC's framework divides remittance providers into distinct categories, each with different responsibilities:

- Remittance network providers operate the network and are responsible for their affiliates' compliance

- Remittance affiliates work under a network provider and must be registered with AUSTRAC separately

- Independent remittance dealers operate standalone and carry full AML compliance obligations themselves

Registration must be renewed every three years, and providers must maintain active AML programs throughout, not just at renewal time. That ongoing obligation is what makes the framework meaningful.

How the U.S. regulates money services businesses:

| Requirement | Detail |

|---|---|

| Registration body | FinCEN (Financial Crimes Enforcement Network) |

| Registration deadline | Within 180 days of starting operations |

| Renewal cycle | Every two years |

| State licensing | Required in most states, separate from federal |

| Surety bonds | Often required at the state level as financial guarantee |

| AML program | Mandatory written program, updated regularly |

FinCEN requires MSB registration within 180 days of launch, with biennial renewal and state-level licensing on top of the federal requirement. That two-layer structure means a provider operating legally in the U.S. has cleared significant regulatory hurdles before they ever process your transfer.

You can also explore the IdealRemit blog for guides on navigating provider requirements in specific transfer corridors.

Transparency and privacy: modern pillars of trust for remittance users

Beyond legal compliance, trust also requires transparency and respect for your privacy. These are areas where even large, well-known providers often fall short in ways that directly affect what you pay and what happens to your personal information.

Consumer Reports' 2026 testing of major remittance apps revealed widespread problems with hidden fees and excessive data collection. Senders often see a low advertised fee but lose money through exchange rate markups that quietly reduce what the recipient receives. That gap between the mid-market rate and the rate offered to you is where many providers make their real profit.

Privacy is just as uneven. Some providers collect far more data than they need for the transfer itself, then share it with third-party marketing partners. That's data about your income, your recipient, and your transfer frequency, used for purposes that have nothing to do with moving your money safely.

Here's what to watch for when evaluating a provider's transparency:

- Fee disclosure before you commit: Total cost including exchange rate markup should be visible upfront

- Delivery time estimates: Specific, reliable windows rather than vague "1-5 business days"

- Data collection scope: What personal information is collected and why

- Third-party sharing policies: Whether your data is shared for marketing purposes

- Opt-out controls: Meaningful ability to limit data sharing

Wise and Remitly scored highest in Consumer Reports' evaluation for both fee transparency and privacy protections. Understanding these differences before you send can meaningfully protect both your money and your personal information. Our guide on how to transfer money securely walks through the practical steps in detail.

Pro Tip: Always check the provider's privacy policy before registering. Look specifically for whether they share your data with "affiliates" or "marketing partners" since that language usually means your information travels widely. You can also review remittance data privacy controls for a baseline understanding of what meaningful data protection looks like.

Reliability and service features that trusted providers deliver

Regulation and transparency matter at the institutional level. But what you actually feel day-to-day is whether your money arrives on time and whether you know what's happening while it's in transit.

The benefits of secure remittance from a trusted provider go beyond just compliance checkboxes. They translate directly into operational features that reduce anxiety for both senders and recipients.

ANZ's 2026 enhancements to international money transfers illustrate what modern trusted providers should offer: transaction monitoring, sanctions screening at the point of transfer, complete audit trails, in-app tracking with estimated delivery times, and advanced fraud detection that flags anomalies before they become problems.

Here's what reliable service from a trusted provider actually includes:

- Real-time transfer tracking so you and your recipient can follow the money

- Accurate delivery time estimates based on corridor, payout method, and bank processing

- Sanctions screening at the time of transfer, not retrospectively

- Automated fraud detection that can pause a suspicious transfer before it completes

- Audit trails that give you documentation if you need to dispute a delayed or failed transfer

- Near real-time settlement for select corridors where payment rails support it

The practical value here is significant. When your recipient is waiting on funds to pay rent or medical bills, knowing your provider has real-time tracking and a predictable delivery window reduces real financial stress. Learn more about how mobile money for global transfers is expanding payout options in emerging markets.

Comparing trusted remittance providers: fees, privacy, and service quality

Having explored how providers compare in principle, here's a structured look at how major providers stack up across the dimensions that matter most to you.

| Provider | Fee transparency | Privacy rating | Payout options | Tracking available |

|---|---|---|---|---|

| Wise | High | Strong | Bank transfer | Yes |

| Remitly | High | Strong | Bank, cash, mobile wallet | Yes |

| Western Union | Moderate | Moderate | Bank, cash, mobile | Yes |

| MoneyGram | Low | Weak | Bank, cash | Limited |

Consumer Reports' 2026 evaluation found that Wise and Remitly performed best across transparency and privacy metrics, while MoneyGram scored lowest on both safety and privacy measures. That ranking has real implications for how your data is handled and how clearly you understand what you're paying.

When comparing providers, look at these factors together rather than in isolation:

- Total cost including both the stated fee and the exchange rate markup applied to your transfer amount

- Privacy policy clarity and whether opt-out options are genuinely accessible

- Payout method availability for your specific recipient's location (not every provider supports mobile wallet delivery in every country)

- Delivery time reliability, meaning how often actual delivery matches the estimate given at checkout

For a specific corridor example of how these factors play out, our breakdown of the best ways to send money from USA to Mexico shows real cost and reliability differences between providers.

Practical tips to ensure your remittance provider is truly trusted

With these tips in hand, you're ready to make decisions based on evidence rather than assumption.

- Verify registration status with the relevant national authority before your first transfer. FinCEN in the U.S., AUSTRAC in Australia, or the FCA in the UK. A simple search takes two minutes and confirms legal compliance.

- Calculate total cost, not just the headline fee. Enter the same transfer amount on two or three platforms and compare what the recipient actually receives after exchange rate markups.

- Confirm payout method availability for your recipient's specific location. Not every provider offers cash pickup or mobile wallet in every city or country.

- Check delivery time estimates and whether they're guaranteed or approximate. Confirming payout timing upfront prevents surprises when your recipient is counting on funds at a specific time.

- Read the privacy policy before creating an account. Look for data sharing with third parties and whether you can limit it.

- Choose providers with active AML and fraud detection programs. These aren't just regulatory requirements. They're the mechanisms that protect your transfer if something goes wrong.

Pro Tip: Use our security checklist for transfers as a printable reference when evaluating any new remittance provider. It covers every verification step in plain language.

Why trust in remittance providers goes beyond brand reputation

Here's the view most remittance marketing won't tell you: brand familiarity is one of the weakest indicators of provider trustworthiness. A company can spend heavily on advertising, have a recognizable logo in airport terminals worldwide, and still maintain weak AML controls or poor privacy practices.

Real trust is an evidence-based checklist. It includes documented compliance records, clear procedures for handling fraud and AML obligations, and transparent payment rail disclosure. FATF's framework makes this explicit: compliance isn't a one-time credential. It's an ongoing demonstrated condition of operation. That distinction matters enormously when your transfer stalls or a payout fails. A provider with a strong compliance framework has documented audit trails, escalation procedures, and regulatory accountability that makes resolving disputes faster and more predictable.

The uncomfortable truth is that many senders choose providers based on comfort and convenience rather than documented trustworthiness. That works fine until it doesn't. When a transfer is delayed for three days and your recipient can't pay a bill, what you want is a provider whose obligation to you is not just moral but legal and documented. Understanding the regulatory framework behind trusted providers in money transfer gives you the vocabulary to ask the right questions and make better choices before a problem happens. The IdealRemit blog covers these frameworks across different corridors and regulatory environments.

Find the best trusted remittance provider for your transfers

Knowing what makes a provider trustworthy is only useful if you can act on it quickly and confidently. IdealRemit is built exactly for that. The platform lets you compare money transfer services side-by-side across fees, exchange rates, payout options, and transfer speeds, so you can see the total cost of any transfer at a glance.

Whether you're sending from the U.S., Europe, or Australia, you can filter money transfer services for your corridor and access the provider options most relevant to your needs. Every service listed on IdealRemit is drawn from licensed, regulated providers. Set up a rate alert, track live exchange rates, and calculate your potential savings before you commit to a transfer.

Frequently asked questions

Why is it important to use a licensed remittance provider?

Licensed providers meet regulatory standards that protect your money from fraud and ensure compliance with anti-money laundering laws, lowering your risk of lost or delayed transfers. All MVTS providers must be licensed and monitored to prevent misuse for illicit finance.

What should I look for to confirm a provider's trustworthiness?

Check for registration with relevant authorities, clear fee disclosure, strong privacy protections, and operational features like real-time tracking. Consumer Reports highlights transparency and privacy as key trust factors across major remittance apps.

How do remittance providers protect against fraud and illegal activity?

They implement AML programs, monitor suspicious transactions, screen against sanctions lists, and train staff to detect threats across all transfer channels. These controls are critical components of every regulated remittance provider's operation.

Can privacy concerns affect my choice of remittance provider?

Yes, providers differ significantly in how much personal data they collect and how broadly they share it. Consumer Reports found wide variance in remittance apps' handling of customer data, making privacy policy review an essential step before signing up.

Recommended

Written by

Brahim Oubrik

Brahim Oubrik, a senior data engineer who experienced firsthand the challenges of sending money internationally. Living in France while supporting his family in Morocco, Brahim regularly needed to transfer funds across borders. Drawing on his background in data engineering, Brahim decided to solve this problem not just for himself, but for the millions of others navigating the same difficulties. He built Ideal Remit to bring clarity to the international money transfer market.