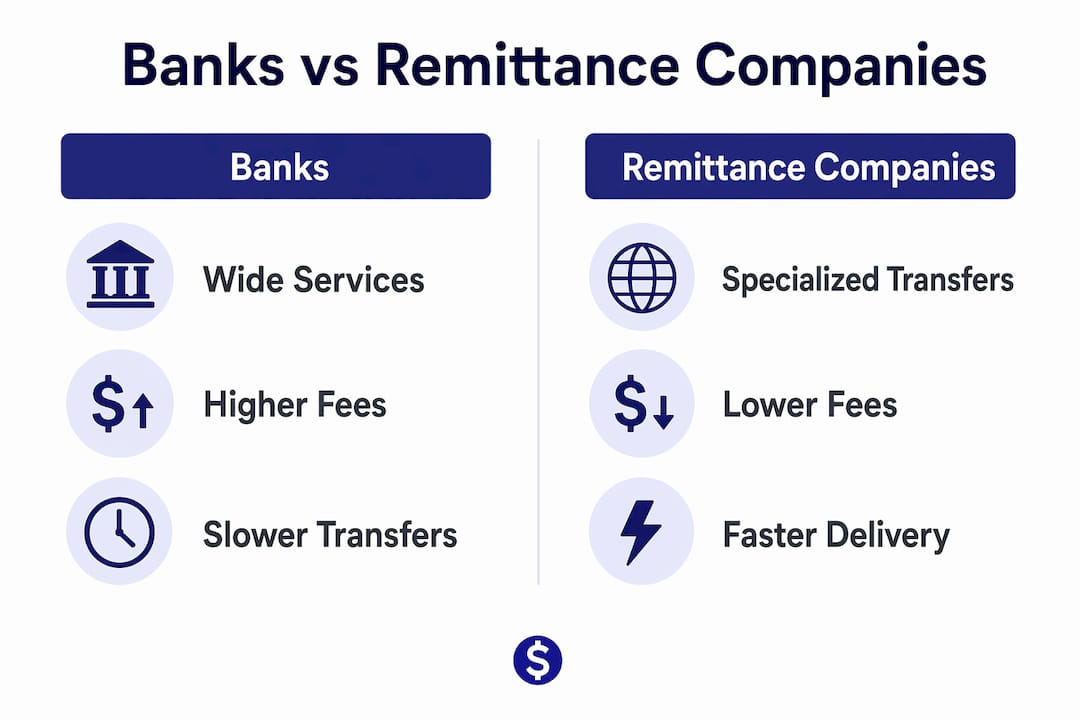

Banks vs Remittance Companies: Key Differences Explained

TL;DR:

- Banks provide broad financial services and face stricter regulation, while remittance companies focus solely on fast, low-cost cross-border transfers under payment regulation. Remittance firms typically charge lower fees, offer faster transfers, and have stronger consumer protections through specific regulatory rules, unlike banks. The emerging hybrid models combine banking credentials with fintech efficiency, making comparison essential for optimal international payment choices.

The difference between banks and remittance companies is this: banks are licensed credit institutions offering deposits, loans, and investment products, while remittance companies are payment service providers built specifically to move money across borders quickly and at lower cost. That distinction shapes everything from the fees you pay to the protections you receive. If you send money internationally through your bank without comparing alternatives, you are almost certainly overpaying. This article breaks down how the two models work, where they diverge on cost and speed, and how to choose the right option for your next transfer.

How do banks and remittance companies differ in how they operate?

The core difference between banks and remittance companies starts at the regulatory level. Banks are licensed credit institutions authorized to accept deposits, extend credit, and offer investment products. Remittance companies, by contrast, are authorized as payment service providers. Their license covers money movement only. They cannot lend you money or hold your savings in a traditional account.

This licensing gap has real consequences for how each type of institution operates:

- Banks answer to central banks and comprehensive banking regulators. They must maintain strict capital reserves and can use customer deposits to fund loans and investments.

- Remittance companies operate under payment services regulations. They are typically required to hold client funds in safeguarded accounts that are kept separate from the company's own operating funds.

- In the UK, for example, the Financial Conduct Authority (FCA) authorizes payment institutions while the Payment Systems Regulator (PSR) oversees payment infrastructure. Banks and remittance firms answer to different parts of this framework.

- In the US, remittance companies register with FinCEN and comply with state money transmitter licenses, while banks fall under the Office of the Comptroller of the Currency (OCC) or the Federal Reserve.

Pro Tip: Before sending money with any provider, verify their authorization status on the FCA register, FinCEN database, or your country's equivalent. An unauthorized provider offers you no regulatory protection if something goes wrong.

The practical result is that banks carry broader financial power but also heavier overhead. Remittance companies carry a narrower mandate, which lets them optimize their entire operation around one task: getting your money from point A to point B as efficiently as possible.

What are the real cost and speed differences?

Cost and speed are where the banks vs remittance services debate becomes most visible to everyday users. Banks often charge higher fees and apply exchange rate margins that quietly inflate the true cost of a transfer. A bank might advertise a $25 wire fee, but the real cost is embedded in the exchange rate spread, which can add another 2% to 4% on top.

Here is a direct comparison of what you can typically expect:

| Factor | Banks | Remittance companies |

|---|---|---|

| Transfer fees | $15 to $50 per wire | $0 to $10 per transfer |

| Exchange rate margin | 2% to 4% above mid-market | 0.5% to 2% above mid-market |

| Transfer speed | 1 to 5 business days | Same day to 1 business day |

| Digital access | Varies by institution | Typically app-first |

| Coverage | Global via SWIFT | 50 to 200+ countries depending on provider |

Bank transfers rely heavily on the SWIFT network. A common misconception is that SWIFT moves money instantly. SWIFT is a messaging network, not a payment rail. The actual settlement depends on correspondent bank relationships, time zones, and manual processing steps at each institution in the chain. That is why a transfer from the US to Morocco can take three to five business days even when both banks are major institutions.

Remittance companies sidestep much of this by using alternative payment rails, pre-funded local accounts, and real-time payment networks in destination countries. Providers like Wise, Remitly, and Western Union have built infrastructure that lets them credit recipients within hours rather than days.

Pro Tip: Always compare the total cost of a transfer, not just the upfront fee. Use a comparison tool that shows you the mid-market exchange rate alongside the provider's rate so you can see the true margin you are paying.

Understanding why exchange rates matter for international transfers is the single most effective way to reduce what you spend on remittances over time.

How do security and consumer protections compare?

Security is often cited as a reason to stick with banks, but the reality is more nuanced. Both banks and licensed remittance companies operate under anti-money laundering (AML) and know-your-customer (KYC) rules. The difference lies in what happens when something goes wrong.

Here is how consumer protections break down by provider type:

- Bank wire transfers offer limited recourse once funds are sent. Most banks will attempt a recall, but there is no guaranteed timeline or refund obligation under US federal law for consumer wire transfers.

- Remittance transfers under the US Remittance Transfer Rule give you a 30-minute cancellation window after initiating a transfer. The provider must refund your money within three business days of a valid cancellation request.

- Error resolution under the Remittance Transfer Rule requires providers to investigate disputes and correct errors, including wrong amounts, wrong recipients, and delays. Banks have no equivalent federal mandate for international wires.

- Safeguarding requirements for licensed remittance companies mean your funds are held in protected accounts. If the company becomes insolvent, those funds are ringfenced from creditors.

- Unauthorized providers offer none of these protections. Confirming provider licensing before transferring is not optional. It is the baseline check that separates a safe transfer from a potential loss.

The key takeaway here is that licensed remittance companies often provide stronger defined consumer protections for international transfers than banks do, precisely because regulators wrote specific rules for this use case. Banks have broader financial protections overall, but those protections were not designed with cross-border consumer remittances in mind.

One practical note: consumer protection timelines are strict. If you spot an error in a remittance transfer, report it immediately. Waiting even a few hours can affect your ability to cancel or claim a refund.

When should you choose a bank versus a remittance company?

The right choice depends on what you are actually trying to accomplish. Neither option is universally better. The decision comes down to transfer size, frequency, destination, and how much the cost matters to you.

Choose a bank when:

- You are sending a large business payment where your existing banking relationship provides added trust and documentation.

- The recipient country has limited remittance infrastructure and SWIFT is the most reliable route.

- You need the transfer integrated with other banking services like letters of credit or escrow.

- You are already paying a monthly fee that includes free or discounted wire transfers.

Choose a remittance company when:

- You send money regularly to family abroad and cost savings compound over time.

- Speed matters and you need funds to arrive the same day or next day.

- The destination is well-served by providers like Remitly, Wise, MoneyGram, or Western Union.

- You want a mobile-first experience with real-time tracking and rate alerts.

A third category is worth knowing about. Hybrid fintech-bank models are increasingly common. These are platforms that partner with licensed banks to combine regulatory trust with fintech-level speed and pricing. Wise, for example, holds banking licenses in multiple jurisdictions while operating with the user experience of a modern app. This blurring of the traditional banks vs remittance services divide means your best option in 2026 may not fit neatly into either category.

The best approach is to check alternatives to bank transfers before defaulting to your bank for any international payment. The savings on a single transfer can be significant. Across a year of regular transfers, they can be substantial.

Key takeaways

Remittance companies consistently outperform banks on cost and speed for personal international transfers, while banks retain advantages for complex, large-scale, or integrated financial transactions.

| Point | Details |

|---|---|

| Service scope differs fundamentally | Banks offer deposits, loans, and investments; remittance companies execute transfers only. |

| Cost advantage favors remittance firms | Banks charge higher fees and wider exchange rate margins than specialized providers. |

| Speed gap is structural | Bank SWIFT transfers take 1 to 5 days; remittance companies often deliver same-day or next-day. |

| Consumer protections are transfer-specific | The US Remittance Transfer Rule gives defined cancellation and refund rights that bank wires lack. |

| Licensing determines your protection | Always verify a provider's authorization before sending funds, regardless of provider type. |

Why the hybrid model changes everything

I have spent years watching people default to their bank for international transfers out of habit rather than logic. The assumption is that a bank is safer and more reliable. That assumption is only partially true, and it costs people real money every month.

What I find most interesting in 2026 is not the gap between banks and remittance companies. It is how fast that gap is closing from the remittance side. Providers are acquiring banking licenses, building compliance infrastructure, and partnering with correspondent banks to extend their reach. The result is that the best remittance platforms now offer the regulatory credibility of a bank with the pricing and speed of a specialist.

The piece most users still miss is the SWIFT misconception. People see "international wire" and assume their bank is using some fast, direct channel. In reality, a transfer from Chicago to Casablanca might pass through two or three correspondent banks, each adding processing time and potentially a fee. Understanding why remittance delays happen is not just academic. It explains why your bank transfer is still "pending" on day three.

My honest advice: use your bank for what it does well, which is managing your savings, credit, and domestic payments. For cross-border transfers, compare your options every time. The market moves fast, and the provider that offered the best rate six months ago may not be the best today. Checking takes two minutes and can save you more than you expect.

— Brahim

Find the best rate for your next international transfer

Idealremit aggregates real-time rates and fees from trusted providers including Western Union, MoneyGram, Remitly, and Wise so you can see exactly what each transfer will cost before you commit. The platform covers transfers to over 100 countries, with transparent fee breakdowns and live exchange rate tracking. You can set personalized rate alerts to send money when conditions favor you, and calculate potential savings against standard bank rates. For anyone sending money abroad regularly, comparing transfer services on Idealremit takes less time than logging into your bank and consistently surfaces better options.

FAQ

What is the main difference between banks and remittance companies?

Banks are licensed credit institutions that offer deposits, loans, and investment products, while remittance companies are payment service providers authorized solely to execute money transfers. This difference in licensing determines their fees, speed, and the consumer protections they must offer.

Are remittance companies safe to use for international transfers?

Licensed and authorized remittance companies are safe. Regulated providers hold client funds in safeguarded accounts separate from operating funds, and in the US, the Remittance Transfer Rule gives consumers defined cancellation and error-resolution rights. Always verify a provider's license before transferring.

Why are bank international transfers slower than remittance services?

Bank transfers rely on the SWIFT messaging network, which routes payments through correspondent banks before settlement. This chain of intermediaries adds processing time, resulting in transfers that take 1 to 5 business days. Remittance companies use alternative payment rails and pre-funded local accounts to deliver funds faster, often within hours.

Can I cancel a remittance transfer if I make a mistake?

Under the US Remittance Transfer Rule, you have a 30-minute window to cancel a transfer and receive a full refund within three business days. This protection applies to personal remittance transfers and does not extend to standard bank wire transfers, which have no equivalent federal cancellation mandate.

When does it make sense to use a bank instead of a remittance company?

Banks are the better choice for large business payments, transfers requiring integrated banking documentation, or destinations where remittance infrastructure is limited and SWIFT is the most reliable route. For regular personal transfers where cost and speed matter, specialized remittance providers almost always offer a better deal.