TL;DR:

- Choosing a provider based on total transfer cost, including exchange rate markups, can save hundreds of dollars annually.

- Funding transfers via bank transfers and timing with rate alerts further reduce expenses, especially for larger sums.

Saving on money transfers means paying attention to the total cost of a transaction, not just the advertised fee. Traditional banks charge $25-$50 flat fees plus 2-5% hidden exchange rate markups, making them the most expensive option by far. Specialist providers like Wise, Remitly, and OFX charge transparent fees of 0.4-1.5%, which translates to real savings on every transfer. The industry term for what you're actually paying is the total transfer cost, which combines upfront fees and the exchange rate spread. This guide breaks down exactly how to reduce that number.

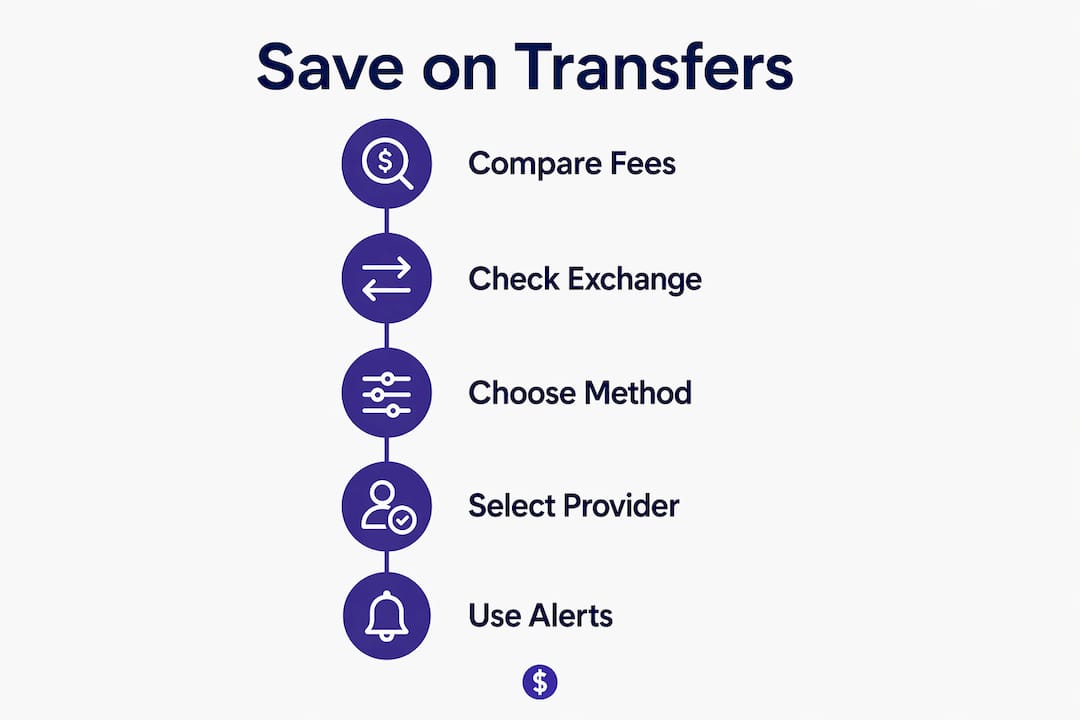

How to save on money transfers by comparing true costs

The biggest mistake senders make is comparing advertised fees instead of the actual amount the recipient receives. A provider charging zero fees can still cost you more than one charging a flat $5, because the difference is buried in the exchange rate.

Understanding exchange rate markups

Every provider sets its own exchange rate. The mid-market rate is the real rate you see on Google or Reuters. Providers mark up that rate and keep the difference as profit. A 2% markup on a $2,000 transfer costs you $40 before you even see a fee line. Hidden exchange rate markups often raise total cost above transparent providers charging flat fees with mid-market rates. That means a "zero fee" transfer can actually cost more than a transfer with a visible $10 charge.

How to find the mid-market rate

Go to Google, type the currency pair you need, and note the rate shown. Then check what rate your provider offers for the same pair. The gap between those two numbers is the markup. Multiply that gap by your transfer amount to see the hidden cost in dollars. This single step reveals more about a provider's true pricing than any fee comparison table.

Comparing providers side by side

The most reliable way to compare is to enter your exact transfer amount on each platform and check the recipient amount, not the fee summary. Banks also charge SWIFT intermediary fees of $7-$25 that specialists avoid through direct payout partnerships. The table below shows how costs differ on a $1,000 transfer to Europe.

| Provider | Upfront Fee | Exchange Rate Markup | Recipient Gets (approx.) |

|---|---|---|---|

| Major U.S. Bank | $35 | 3-4% | ~$925 |

| Wise | $6 | 0.4-0.6% | ~$988 |

| Remitly (promo) | $0 | 0.5-1% | ~$990 |

| OFX | $0 | 0.8-1.2% | ~$982 |

The difference between a bank and a specialist on a single $1,000 transfer can exceed $60. Over a year of monthly transfers, that adds up to more than $700.

Pro Tip: Always enter your exact transfer amount on the provider's site and look at the "recipient gets" field before confirming. That number is the only figure that matters.

What payment methods save you the most money?

How you fund a transfer affects the total cost just as much as which provider you choose. The wrong funding method can add 1-3% before the transfer even starts.

- Bank transfer (ACH or wire): The cheapest funding method. Funding by bank transfer avoids the 1-3% surcharges common with credit and debit cards. ACH transfers in the U.S. are typically free and process within one business day.

- Debit card: Convenient but often carries a 0.5-1.5% surcharge on top of the transfer fee. Use only when speed is critical and the surcharge is clearly disclosed.

- Credit card: The most expensive funding method. Card surcharges of 1-3% apply, and your card issuer may also charge a cash advance fee. Avoid this option for regular transfers.

- Pre-loaded multi-currency balance: Platforms like Wise allow you to hold funds in multiple currencies. Converting in advance when rates are favorable locks in a better rate and avoids last-minute markups.

- Cash-to-cash transfers: Services like Western Union and MoneyGram offer cash pickup, but the fees and exchange rate markups are significantly higher than digital alternatives. Reserve this method for recipients without bank access.

Delivery speed also affects cost. Express transfers that arrive in minutes cost more than economy transfers that settle in 1-3 business days. Choosing economy over express can save 1-3% of the transfer amount. For a $3,000 transfer, that's up to $90 saved by waiting an extra day.

Pro Tip: If your recipient does not need the money immediately, select the slowest available delivery tier. The savings function like a guaranteed return on the amount you're sending.

Which provider is best for your transfer amount?

The cheapest provider depends on volume. Promotions dominate for small amounts, specialists win for mid-range transfers, and large transfers require a different approach entirely.

Small transfers under $500

Remitly frequently offers zero fees with near-mid-market rates for first-time users. These promotional rates make Remitly the cheapest option for small or occasional transfers, especially to popular corridors like Mexico, the Philippines, and India. Once the promotion expires, compare again before your next transfer.

Mid-range transfers from $500 to $10,000

Wise is the strongest performer in this range. Its fee structure of 0.4-0.6% plus a small fixed charge consistently delivers more to recipients than banks or cash services. Savings can reach $25-$80 per $1,000 compared to bank wire transfers. For a small business sending $5,000 monthly, switching from a bank to Wise can save over $3,000 per year.

Large transfers over $10,000

OFX and XE specialize in large transfers and negotiate tighter exchange rate spreads for high-volume senders. Both platforms offer dedicated account managers who can lock in rates for future transfers. The low-cost transfer providers that work best for large amounts often charge no upfront fee but earn a small margin on the exchange rate, which is still far below what banks charge.

| Transfer Amount | Best Provider Type | Estimated Savings vs. Bank |

|---|---|---|

| Under $500 | Remitly (promo) or Wise | $10-$25 |

| $500-$10,000 | Wise, Remitly | $25-$80 per $1,000 |

| Over $10,000 | OFX, XE | $100-$400+ per transfer |

Consolidating transfers also reduces costs. Sending one $2,000 transfer instead of four $500 transfers cuts the number of fixed fees you pay. For small businesses with predictable payroll or supplier payments, batching transfers is one of the simplest ways to lower transfer costs.

How do rate alerts help you reduce transfer costs?

Exchange rates move every day, and sometimes every hour. A rate that looks acceptable on Monday may be 1-2% worse by Thursday. Timing your transfers around favorable rates is one of the most underused strategies for cheap international money transfers.

Here is how to use rate alerts effectively:

- Find your target rate. Check the mid-market rate for your currency pair and decide on a rate that represents a fair or favorable level for your transfer.

- Set an alert on your chosen platform. Wise, OFX, and XE all offer rate alert features that notify you by email or app when your target rate is reached.

- Monitor weekly patterns. Currency markets tend to be more active during overlapping banking hours between major financial centers. Rates during low-liquidity periods, such as late Friday afternoons, can be less favorable.

- Act when the alert triggers. Have your transfer details ready so you can execute quickly. Rates can reverse within hours.

- Review your alerts quarterly. Market conditions shift. A rate that seemed ambitious six months ago may now be routine.

A practical example: a small business owner sending $4,000 monthly to a supplier in Europe sets a rate alert on OFX at 1% above the current mid-market rate. When the alert fires three weeks later, the transfer saves approximately $40 compared to sending at the original rate. Over 12 months, that discipline adds up to nearly $500 in savings with no extra effort.

Pro Tip: Combine rate alerts with economy delivery tiers. You get both the timing advantage and the speed discount at the same time.

Key takeaways

The most effective way to reduce money transfer costs is to compare total recipient amounts across specialist providers, fund transfers by bank transfer, and use rate alerts to time larger transactions.

| Point | Details |

|---|---|

| Compare recipient amounts | Always check what the recipient actually receives, not just the advertised fee. |

| Avoid bank wire transfers | Specialists charge 0.4-1.5% vs. banks charging 3-5% plus hidden SWIFT fees. |

| Match provider to transfer size | Use Remitly for small amounts, Wise for mid-range, and OFX or XE for large transfers. |

| Fund by bank transfer | Paying by ACH avoids the 1-3% card surcharge that inflates total cost. |

| Use rate alerts | Setting alerts on Wise, OFX, or XE lets you transfer at favorable rates automatically. |

What i've learned after years of watching people overpay

Most people overpay on international transfers not because they are careless, but because the pricing is deliberately confusing. The "zero fee" marketing that dominates the industry is the single biggest source of unnecessary cost I see. Providers know that customers fixate on the fee line and ignore the exchange rate. That asymmetry is where the money goes.

My honest recommendation is to use at least two providers. Keep one account with a promotional service like Remitly for small, fast transfers where the promo rate makes it genuinely cheap. Keep a second account with Wise or OFX for larger, less urgent transfers where the exchange rate margin matters more. This split approach consistently outperforms any single-provider strategy.

The other mistake I see constantly is treating a transfer setup as permanent. Markets change, providers update their fee structures, and new competitors enter the market. The provider that was cheapest for your corridor 18 months ago may not be cheapest today. I check comparison tools at least once a quarter, and I recommend you do the same. The exchange rate impact on your total cost is not static. It shifts with market conditions and provider pricing decisions.

One more thing: always read the delivery time and recipient fee disclosures before confirming. Some providers advertise a great rate but charge a receiving bank fee that the recipient absorbs. That fee never shows up in your cost calculation, but it reduces what your recipient actually gets.

— Brahim

Find the cheapest transfer in seconds with Idealremit

Idealremit aggregates real-time rates and fees from top providers including Wise, Remitly, OFX, Western Union, and MoneyGram, so you can see the full cost picture in one place. Every comparison shows the recipient amount, not just the fee, which is the only number that tells you the true cost of a transfer.

Whether you send $200 to family abroad or $15,000 to an overseas supplier, Idealremit calculates your potential savings against bank rates and shows you which provider delivers the most. The platform supports transfers to over 100 countries and lets you set personalized rate alerts so you never miss a favorable window. Compare live transfer rates now and see exactly how much you can save on your next transfer.

FAQ

What is the cheapest way to send money internationally?

Specialist online providers like Wise, Remitly, and OFX are consistently cheaper than banks, charging 0.4-1.5% compared to the 3-5% total cost typical of bank wire transfers. The cheapest option for your specific transfer depends on the amount, destination, and whether promotional rates apply.

Why do zero-fee transfers still cost money?

Zero-fee providers recover their revenue through exchange rate markups above the mid-market rate. Advertised zero-fee transfers often cost more in total than providers charging a transparent flat fee with a rate close to mid-market.

How much can i save by avoiding my bank?

Switching from a bank to a specialist provider saves roughly $25-$80 per $1,000 transferred. On a $5,000 monthly business transfer, that represents potential annual savings of $1,500-$4,800 depending on the corridor and provider.

Does the payment method affect my transfer cost?

Yes. Funding a transfer with a credit or debit card adds a 1-3% surcharge that banks and specialist providers both apply. Using an ACH bank transfer as the funding source eliminates that surcharge entirely.

How do rate alerts work for money transfers?

Rate alerts notify you when your target exchange rate is reached on platforms like Wise, OFX, or XE. Setting an alert lets you time transfers at favorable rates rather than sending at whatever rate happens to be available when you log in.