TL;DR:

- The ICICI exchange rate used by Money2India adds a markup of 1%-2.5% over the mid-market rate, affecting the amount received in India. Combining large transfers above $1,000 with rate alerts can help maximize the rupees your family receives. Verifying the actual rate with the FIRA document ensures transparency and protects your transfer value.

The ICICI exchange rate applied by Money2India defines the conversion value you receive when sending money to India, with typical margins of 1%-2.5% above the mid-market rate plus nominal transfer fees. For expatriates and immigrants who send money home regularly, that margin is not a footnote. It is the difference between your family receiving full value or losing a meaningful slice of every transfer. This guide breaks down how the ICICI exchange rate for Money2India works in 2026, what it actually costs you, and how to get more rupees for every dollar you send.

How does ICICI Money2India determine exchange rates and fees?

Money2India sets its exchange rates by adding a markup to the mid-market rate, which is the benchmark rate banks use to trade currencies among themselves. That markup typically runs 1%-2.5% above the mid-market rate, depending on the transfer amount and market conditions. The mid-market rate is what you see on Google or Reuters. The rate you actually get is always lower.

The fee structure is straightforward. Transfers below $1,000 carry a $4 flat fee. Transfers of $1,000 and above are fee-free. That threshold matters because the $4 fee on a $500 transfer represents 0.8% of your principal before the exchange rate spread even applies.

Rates are also slab-dependent. The platform applies slightly better exchange rates at higher transfer volumes. This tiered model rewards senders who consolidate transfers rather than sending smaller amounts frequently.

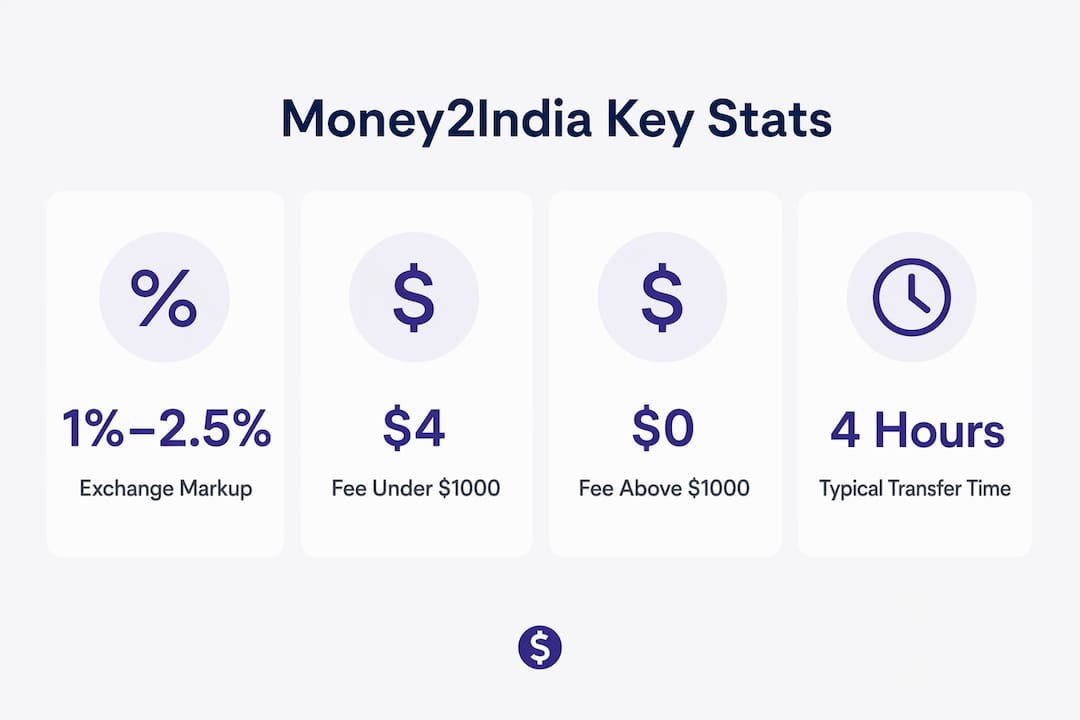

Key facts about the Money2India fee and rate structure:

- Exchange rate markup: 1%-2.5% above the mid-market rate

- Transfer fee: $4 for transfers under $1,000; $0 for $1,000 and above

- Rate type: Slab-based, with better rates at higher amounts

- Delivery to ICICI accounts: Typically within 4 hours

- Delivery to other Indian banks: 1-2 business days via NEFT

Pro Tip: Always transfer at least $1,000 in a single transaction. You eliminate the $4 fee and qualify for the slab rate that applies to the $1,001-$5,000 tier, which is more favorable than the entry-level rate.

What are the real costs of sending money via Money2India?

The published rate on Money2India's website is an indicative rate. It is not the rate locked in for your transfer. The actual conversion rate is applied at the moment of processing, which means intraday currency movements and internal bank spreads can shift what you receive. Senders frequently notice a gap between the rate shown at initiation and the rate confirmed on their receipt.

Understanding hidden costs in exchange rates is the first step to protecting your transfer value. The markup is not listed as a separate line item. It is baked into the rate itself, which makes it easy to overlook.

Here is what that markup costs on common transfer amounts:

| Transfer Amount (USD) | Markup Range | Approximate INR Lost vs. Mid-Market |

|---|---|---|

| $1,000 | 1%-2.5% | ₹750 - ₹1,875 |

| $5,000 | 1%-2.5% | ₹3,750 - ₹7,500 |

| $10,000 | 1%-2.5% | ₹7,500 - ₹15,000 |

On a $5,000 transfer, the markup alone can cost you between ₹3,750 and ₹7,500 compared to the mid-market rate. That is real money, not a rounding error.

"The rate shown during transfer initiation is indicative only. The real rate is applied at conversion time and includes ICICI Bank's internal markup. Always verify the final rate using your Foreign Inward Remittance Advice (FIRA) document after the transfer completes."

The Foreign Inward Remittance Advice, or FIRA, is an official document issued by the receiving bank in India. It confirms the exact exchange rate applied to your transfer. Requesting your FIRA after each transaction is the only reliable way to verify that the rate you received matches what was quoted. Senders who skip this step often discover discrepancies only when they compare multiple transfers over time.

Intraday volatility adds another layer of uncertainty. The USD/INR pair can move by 0.3%-0.5% within a single trading session. If your transfer processes during a period of rupee weakness, you receive fewer rupees than the morning rate suggested. Timing matters more than most senders realize.

How can you optimize your Money2India transfers using slab rates and rate alerts?

The most direct way to improve your effective exchange rate is to use the slab structure deliberately. Money2India publishes tiered rates, and the difference between slabs is real. In March 2026, the platform offered 93.76 INR per USD for transfers up to $5,000, and 93.85 INR per USD for transfers in the $5,001-$10,000 range. That 0.09 INR difference adds up to ₹900 on a $10,000 transfer, simply by crossing the slab threshold.

Practical steps to get better rates on every transfer:

- Consolidate transfers. Send one larger transfer instead of several small ones. You cross into better slab tiers and eliminate the $4 fee on sub-$1,000 amounts.

- Use the rate alert feature. Money2India lets you set a target rate and receive a notification when the market hits that level. This removes the guesswork from timing.

- Avoid festive season peaks. Demand for remittances spikes around Diwali and other major Indian festivals. Higher demand can push spreads wider as providers adjust rates.

- Transfer during stable market hours. The USD/INR rate is most stable during the overlap of US morning hours and Indian afternoon hours. Avoid initiating transfers during high-volatility news events.

- Check the FIRA after every transfer. Confirming the applied exchange rate via FIRA builds a record of what you actually received, which helps you identify patterns and negotiate if you have a relationship with the bank.

Pro Tip: Set your rate alert 0.5%-1% above the current rate. This captures meaningful upside without waiting indefinitely for an unrealistic target. Pair this with a calendar reminder to review your alert monthly, since market conditions shift and your target may need updating.

The role of exchange rates in remittances is often underestimated. A 1% improvement in your effective rate on a $10,000 annual transfer saves roughly $100 per year. Over five years, that is $500 in additional value reaching your family in India.

What delivery speeds and service charges can you expect with Money2India?

Delivery speed is one of Money2India's genuine strengths. Transfers to ICICI Bank accounts in India typically arrive within 4 hours of processing. That is faster than most wire transfer services, which take 1-3 business days. For senders whose family members bank with ICICI, this speed advantage is significant.

Transfers to non-ICICI Indian banks travel via NEFT and take 1-2 business days. NEFT processes in batches, so the exact arrival time depends on when your transfer enters the processing queue. Weekend and holiday delays apply to NEFT transfers, which is worth factoring in when timing is critical.

A summary of what to expect on delivery and fees:

- ICICI-to-ICICI transfers: Arrive within 4 hours in most cases

- ICICI-to-other-bank transfers: 1-2 business days via NEFT

- Fee for transfers under $1,000: $4 flat fee

- Fee for transfers of $1,000 and above: Zero transfer fees, regardless of amount

- Customer support: Available via phone and online chat for US-based senders

The zero-fee threshold at $1,000 is a meaningful incentive. For senders who regularly transfer amounts just below that level, shifting to a single $1,000 transfer instead of two $500 transfers saves $8 per month, or $96 per year, before any exchange rate benefit is counted.

Key Takeaways

The ICICI exchange rate for Money2India transfers includes a 1%-2.5% markup over the mid-market rate, and senders who consolidate transfers above $1,000 and use rate alerts consistently receive better value.

| Point | Details |

|---|---|

| Exchange rate markup | ICICI applies a 1%-2.5% margin above the mid-market rate on every transfer. |

| Fee threshold | Transfers of $1,000 and above carry zero fees; transfers below $1,000 cost $4. |

| Slab-based pricing | Higher transfer amounts unlock marginally better exchange rates per USD. |

| Rate alert feature | Setting a target rate notification helps you time transfers during favorable market conditions. |

| FIRA verification | Always request your Foreign Inward Remittance Advice to confirm the exact rate applied. |

Why I think most expats leave money on the table with Money2India

I have watched a lot of expats treat Money2India as a set-and-forget service. They log in, enter the amount, and hit send without checking the slab tier, the rate alert, or the FIRA afterward. That habit is expensive.

Money2India is genuinely well-suited for ICICI account holders and NRIs who value reliability over chasing the absolute lowest rate. The 4-hour delivery to ICICI accounts is hard to beat. The brand trust is real. But "reliable" does not mean "cheapest," and conflating the two costs senders real rupees every month.

The rate alert feature is the most underused tool on the platform. Most senders I have spoken with have never set one. They send when they need to, at whatever rate is available that day. The alert feature exists precisely to break that habit. It shifts you from reactive to deliberate, and that shift alone can improve your effective rate by 0.5%-1% over a year.

My honest recommendation: use Money2India for its speed and convenience, especially if your recipient banks with ICICI. But always compare the current Money2India rate against the mid-market benchmark before you send. The gap between what you see on Google and what Money2India offers is your real cost. Know that number before you commit. And check your FIRA every single time.

- Brahim

How Idealremit helps you find better rates than Money2India

Knowing the ICICI exchange rate is only half the picture. The other half is knowing whether a better rate exists for your specific transfer amount and destination.

Idealremit aggregates live exchange rates and fees from a wide network of trusted remittance providers, so you can compare transfer services side by side in seconds. You see the real cost of each option, not just the headline rate. Whether you send $500 or $10,000 to India, Idealremit shows you which provider delivers the most rupees for your dollar on that exact amount. Checking takes less than a minute and costs nothing. The savings can be substantial.

FAQ

What is the ICICI Money2India exchange rate markup?

ICICI Money2India applies a markup of 1%-2.5% above the mid-market rate. On a $5,000 transfer, that markup can cost between ₹3,750 and ₹7,500 compared to the mid-market rate.

How do I check the current exchange rates on Money2India?

Log in to the Money2India platform and enter your transfer amount. The rate displayed is indicative and slab-dependent, so the exact rate applied may differ slightly at the time of conversion.

Does Money2India charge transfer fees?

Transfers of $1,000 and above carry zero transfer fees. Transfers below $1,000 incur a flat $4 fee.

How long does a Money2India transfer take to arrive?

Transfers to ICICI Bank accounts in India typically arrive within 4 hours. Transfers to other Indian banks via NEFT take 1-2 business days.

What is a FIRA and why does it matter?

A Foreign Inward Remittance Advice (FIRA) is an official document from the receiving bank in India confirming the exact exchange rate applied to your transfer. Requesting it after each transfer is the only reliable way to verify you received the rate you were quoted.