TL;DR:

- Remittances to Africa exceeded $100 billion in 2022, serving as a vital source of income for households and economies. They support basic needs, incentivize financial inclusion, and promote economic diversification and stability. Reducing transfer costs and using formal, digital methods can maximize long-term benefits for families and national development.

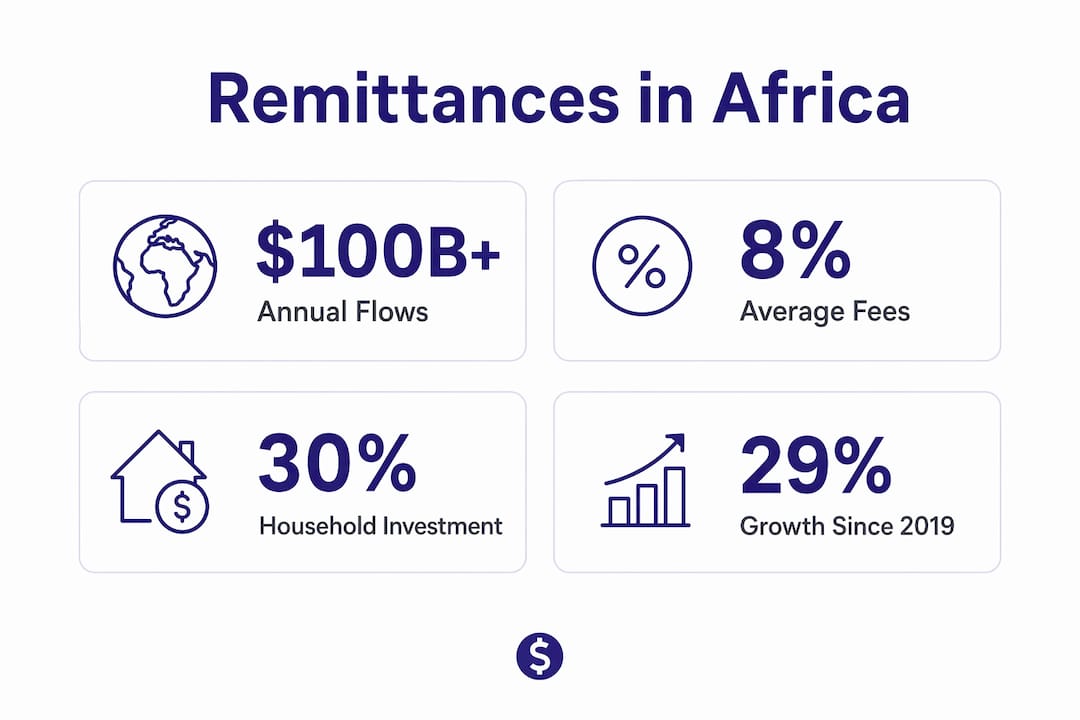

Remittances to Africa are defined as money transfers sent by African diaspora workers to family members and communities back home. Remittance inflows exceeded $100 billion in 2022 and grew by nearly 29% between 2019 and 2023. That scale puts remittances on par with foreign aid and foreign direct investment as a source of external finance for the continent. For millions of households across Sub-Saharan Africa, North Africa, and the Horn of Africa, money sent home is not a supplement. It is the primary financial lifeline. Understanding why send remittances to Africa matters means looking at both the personal motivations and the broader economic forces these transfers set in motion.

Why send remittances to Africa: the household case

The most direct answer is survival and stability. Families receiving money from abroad use it to cover food, rent, school fees, and medical bills that local incomes cannot reliably fund. These are not discretionary purchases. They are the baseline costs of a dignified life.

The economic impact goes further than basic consumption. Up to 30% of receiving households invest remittances in microenterprises, while 35% direct funds toward education and healthcare. That means money sent home does not just feed families today. It builds human capital and small businesses that generate income for years.

Financial inclusion is another concrete benefit. Receiving remittances increases the likelihood of owning a bank or mobile money account by 5-15 percentage points. That shift matters enormously in regions where most adults have historically operated outside the formal financial system. A mobile wallet opened to receive a transfer becomes a tool for saving, borrowing, and paying bills.

Community stability is the third layer. When households have reliable income, local markets stay active, schools retain students, and health clinics see patients who can actually pay. Remittances act as a distributed social safety net that no government program currently replicates at scale.

- Basic needs: Food, housing, and utilities are the first priority for most recipient households.

- Education and health: 35% of remittance spending goes directly to school fees, tuition, and medical costs.

- Microenterprise investment: Nearly one in three households uses funds to start or grow a small business.

- Financial inclusion: Account ownership rises significantly among remittance recipients, reducing cash dependency.

- Community stability: Consistent income flows keep local economies active even during regional downturns.

Pro Tip: If you send money regularly, consider splitting transfers into two purposes: one portion for immediate household needs and one earmarked for a savings goal or small business investment. This simple habit turns a monthly obligation into a long-term asset.

How do remittances shape Africa's broader economic development?

Beyond individual households, remittances function as a macroeconomic stabilizer. Unlike foreign aid, which depends on donor politics, or foreign direct investment, which chases profit opportunities, remittances flow consistently because family obligation does not pause during recessions or political crises. Remittances provide up to 50% of external development finance in fragile and conflict-affected contexts. That reliability is what makes them structurally different from other capital flows.

Economic diversification is a less obvious but equally important benefit. Empirical research shows that remittances significantly drive economic complexity in Sub-Saharan Africa by providing households with capital to invest outside struggling commodity sectors. A farmer who receives regular transfers can afford to send a child to vocational school, fund a small retail shop, or purchase equipment that increases productivity. These individual decisions, multiplied across millions of households, shift the economic structure of entire regions.

Domestic savings mobilization is the third channel. When remittances flow into formal accounts, banks gain deposits they can lend to local businesses. That lending creates jobs and expands the tax base. The connection between a diaspora worker's monthly transfer and a local entrepreneur's business loan is real, even if it is rarely discussed.

Remittances are not charity. They are a form of distributed investment that, when channeled through formal financial systems, can fund the economic transformation that aid programs have long promised but rarely delivered. The next step is moving from consumption support to structured instruments like diaspora bonds and regulated investment funds.

- Stability over volatility: Remittances remain consistent even when foreign investment retreats during economic downturns.

- Diversification capital: Households invest beyond commodity sectors, building economic complexity at the local level.

- Savings mobilization: Formal account deposits from remittances expand the lending capacity of local banks.

- Diaspora finance potential: Structured diaspora finance tools like bonds and regulated funds can convert personal transfers into national development instruments.

What challenges affect sending remittances to Africa?

The single biggest obstacle is cost. The average cost of sending money to Africa sits at about 8% per transaction. The United Nations Sustainable Development Goal target is 3%. Africa carries the highest regional transfer costs in the world, and that gap represents billions of dollars that never reach recipient households each year.

Regulatory fragmentation compounds the problem. Each country operates under different licensing requirements, anti-money-laundering rules, and correspondent banking relationships. Providers must navigate this patchwork to offer legal services, and those compliance costs get passed on to senders.

Exchange rate distortions create a separate trap. In countries with dual exchange rate systems, capital controls push senders toward informal channels because recipients get more local currency through unofficial networks. The short-term gain for the recipient comes with real risks: no consumer protection, no recourse if the transfer fails, and no contribution to the formal financial system.

| Challenge | Impact on senders and recipients |

|---|---|

| High transfer costs (avg. 8%) | Reduces the amount received; costs nearly triple the UN SDG target of 3% |

| Regulatory fragmentation | Limits provider access; raises compliance costs passed to users |

| Dual exchange rates | Incentivizes informal channels with higher risk and no consumer protection |

| De-risking by banks | Reduces formal banking access for remittance corridors, limiting competition |

Pro Tip: Always compare the total cost of a transfer, not just the fee. The exchange rate markup is often where providers recover the most margin. Use a transfer comparison tool to see the full cost before you send.

How can senders and recipients maximize the benefits of remittances?

Digital and mobile money platforms offer the clearest path to lower costs and faster delivery. These platforms operate with lower overhead than traditional bank wire services and pass some of those savings to users. For recipients in countries with strong mobile money infrastructure, funds arrive within minutes and are immediately usable for purchases and bill payments.

Staying within formal channels is not just about cost. It is about protection. Formal transfers are traceable, insured against provider failure in most jurisdictions, and contribute to the recipient's financial record. That record matters when they later apply for credit or a mortgage. Remittances through formal channels build the financial identity that informal networks never can.

Remittance-backed financial products are an underused option. Housing savings plans and direct utility bill payments funded by regular transfers reduce inflation exposure and create tangible assets. Instead of sending cash that gets spent immediately, a sender can direct funds to a structured savings account or pay a family member's electricity and water bills directly. The money achieves the same purpose with less leakage.

The emotional dimension also shapes behavior. The phenomenon known as "Black Tax" describes the social pressure many diaspora workers feel to support extended family networks beyond their immediate means. Recognizing this pressure as a real financial planning factor, rather than a personal failing, helps senders set sustainable limits and communicate them clearly.

- Use digital platforms: Mobile money transfers typically cost less and arrive faster than bank wire services.

- Stay formal: Formal channels build recipient financial records and provide consumer protection.

- Direct bill payments: Pay utilities, school fees, or insurance premiums directly to reduce cash leakage.

- Set clear limits: Acknowledge the social pressure of Black Tax and establish a sustainable sending budget.

- Track delays: Understand why transfers get delayed so you can plan around them and avoid emergencies.

Key Takeaways

Remittances to Africa are the continent's most reliable external financial flow, and reducing transfer costs from 8% toward the UN SDG target of 3% would unlock billions in additional household income each year.

| Point | Details |

|---|---|

| Scale of remittances | Flows exceeded $100 billion in 2022 and grew 29% from 2019 to 2023. |

| Household impact | 35% of funds go to education and health; 30% fund microenterprise investment. |

| Financial inclusion | Receiving remittances raises formal account ownership by 5-15 percentage points. |

| Cost barrier | The average 8% transfer cost is nearly triple the UN SDG 3% target, reducing recipient value. |

| Maximizing impact | Formal channels, digital platforms, and remittance-backed products increase the long-term benefit of every transfer. |

Remittances are bigger than money: a perspective from the field

I have spent years watching the conversation about African development focus on aid budgets and foreign investment deals. Remittances rarely get the same attention in policy rooms, yet they move more money and reach more people than most official programs ever will.

What strikes me most is the efficiency gap. A diaspora worker in London or Houston sends $200 home, and $16 disappears in fees before the family sees a cent. That is not a minor inconvenience. Across millions of transfers, it is a structural tax on people who can least afford it. Closing that gap does not require a new aid program. It requires better tools, more competition among providers, and governments willing to simplify the regulatory environment.

The Black Tax dimension is something I think the financial industry handles badly. Providers market remittances as a feel-good act of generosity. The reality for many senders is closer to a monthly obligation that competes with their own rent and retirement savings. Honest financial planning for diaspora workers has to account for that pressure, not pretend it does not exist.

The most exciting shift I see is the move toward structured diaspora finance. When remittances fund diaspora bonds or regulated investment vehicles, they stop being a private transfer and become a development tool with scale. Africa does not need more charity. It needs its own diaspora to invest in it with the same confidence they invest in their host countries.

- Brahim

Idealremit makes comparing transfer costs straightforward

Sending money to Africa should not mean accepting high fees or guessing which provider offers the best rate today.

Idealremit is a comparison platform that aggregates real-time rates and fees from a wide network of trusted transfer services, so you can see the full cost of a transfer before you commit. The platform supports transfers to over 100 countries, with strong coverage across Africa. You can set rate alerts, track live exchange rates, and calculate exactly how much your recipient will receive. Compare transfer services now and find the most affordable option for your next transfer to Africa.

FAQ

What are remittances to Africa?

Remittances to Africa are money transfers sent by African diaspora workers living abroad to family members and communities in their home countries. These flows exceeded $100 billion in 2022 and represent one of the continent's largest sources of external finance.

Why are remittances important for African families?

Remittances fund basic needs like food, housing, healthcare, and school fees that local incomes often cannot cover. Around 35% of remittance spending goes directly to education and health, making these transfers a critical household resource.

How much does it cost to send money to Africa?

The average cost of sending money to Africa is about 8% per transaction, the highest of any region globally. The UN Sustainable Development Goal target is 3%, meaning most senders currently pay nearly triple what they should.

How do remittances help reduce poverty in Africa?

Remittances reduce poverty by providing reliable income to households, funding microenterprise investment, and increasing access to formal financial services. Recipients are 5-15 percentage points more likely to own a bank or mobile money account, which expands their economic options.

What is the best way to send money to Africa?

Digital and mobile money platforms typically offer lower fees and faster delivery than traditional bank wire services. Using a comparison tool like Idealremit helps senders identify the lowest total cost, including both fees and exchange rate markups.